[ad_1]

There’s an outdated Chinese language curse that claims “Could he reside in fascinating instances.” Prefer it or not, we reside in fascinating instances. COVID is receding however not gone, and whereas markets have rebounded properly from the disaster (the S&P 500 is up 19% up to now this 12 months), the overall financial system is displaying some worrisome indicators. Jobs creation slowed in August, and employers reported over 11 million unfilled positions – however unemployment, whereas ticking down, stays above 5%. Extra ominously, in a sign that provide chains and distribution networks haven’t recovered from the pandemic disruptions, a document 65+ container ships are caught off the Port of Lengthy Seaside ready to unload.

So what to make of those conflicting alerts? Ought to traders keep away from the market, or dive in headfirst? Watching the scene from Oppenheimer, chief funding strategist John Stoltzfus believes that the present setting resembles previous crises which have come and gone, leaving of their wake winners among the many bulls.

“At any time when the posh of hindsight for current instances (i.e. the Pandemic Disaster) lastly arrives traders could come to understand that certainly historic priority reveals that instances of disaster, if efficiently managed and navigated by financial coverage makers, companies, and customers, will be certainly good instances for traders of many stripes together with merchants, intermediate time period and longer-term traders,” Stoltzfus wrote.

Taking Stoltzfus’ outlook into consideration, we needed to take a more in-depth take a look at three shares getting a spherical of applause from Oppenheimer. Because the agency’s analysts suppose every may surge over 50%, we used TipRanks’ database to search out out much more concerning the trio.

Clarus Therapeutics (CRXT)

Metabolic ailments and hormonal problems type a severe class of diseases and are notoriously troublesome to deal with. Clarus is engaged on assembly the wants of sufferers with these problems, by means of the event of metabolic therapies and androgen alternative. The corporate has one product, Jatenzo, which has been authorized as a remedy for hypogonadism, and 4 further drug candidates in pre-clinical testing for quite a lot of metabolic purposes.

Jatenzo is the primary – and for now, the one – oral softgel capsule for testosterone alternative remedy. It acquired FDA approval for the remedy of male hypogonadism again in 2019, however introduction to the US market was held up by patent litigation with Lipocine. The litigation, involving mental property and patent interference, has been settled by settlement between the events as of this previous June. The phrases are sealed, however don’t contain monetary funds by Clarus – and the best way is now clear for commercialization of the drug.

This firm had one different main piece of reports this summer time, when in early September it introduced the closing of its enterprise mixture with Blue Water Acquisition, a SPAC entity. The mix merged the businesses and noticed the CRXT ticker begin buying and selling on the NASDAQ on September 10. Clarus gained $25.3 million in gross proceeds from the SPAC transaction.

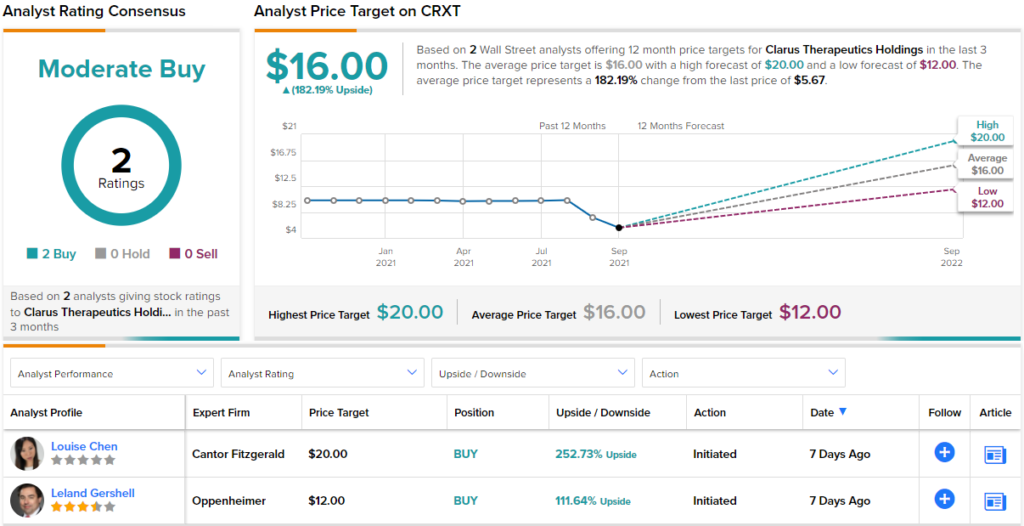

Among the many healthcare title’s followers is Oppenheimer’s Leland Gershell. The analyst charges CRXT an Outperform (i.e. Purchase), and his $12 value goal implies an upside of ~112% for the 12 months forward. (To look at Gershell’s monitor document, click on right here)

“With twice-daily capsule Jatenzo, Clarus brings a first-in-class oral choice to ~2.2M US males who obtain testosterone alternative merchandise. We count on Jatenzo will take rising share from topical and injectable mainstays in addition to improve general remedy charges among the many ~6M US males recognized w/low testosterone. Alongside industrial execution, CRXT is actively pursuing once-daily improvement, indication enlargement, and ex-US markets. In girls’s well being, lately in-licensed candidate CLAR-121 has potential to handle breast illness (irritation, most cancers). Buying and selling at a $[125M] enterprise worth and with ~one 12 months of money on the steadiness sheet, we count on shares to Outperform as Jatenzo’s launch builds steam,” Gershell opined.

The Oppenheimer view is certainly one of two optimistic critiques on document for Clarus, giving the inventory its Average Purchase consensus ranking. Share are buying and selling for $5.67 and their common goal of $16 is much more bullish than Gershell allowed, suggesting a strong upside of 182% within the subsequent 12 months. (See CRXT inventory evaluation on TipRanks)

Denali Therapeutics (DNLI)

Subsequent up is Denali Therapeutics, a scientific stage biopharma firm with a particular concentrate on neurodegenerative ailments. The corporate is engaged on a rating or extra of drug candidates, with most in early preclinical improvement – however 5 candidates have begun human scientific trials. The drug candidates are engineered small molecules designed to cross the blood-brain barrier, and the focused ailments embody Alzheimer’s, ALS, Parkinson’s, and lupus, amongst others.

In the previous couple of months, Denali has reported a number of milestones in its scientific trial applications. A Section 1/1b research of DNL151, a possible remedy for Parkinson’s, met its security targets and is on monitor for mid-stage scientific trials by the top of this 12 months. Additionally this previous summer time, DNL310, being investigated in sufferers with Hunter syndrome, confirmed optimistic knowledge in its Section 1/2 research. The information demonstrated a sturdy CNS impact of the drug candidate, together with a suitable security profile. The corporate is planning an additional scientific trials of DNL310 within the first half of subsequent 12 months.

In a considerably extra superior trial stage, DNL758 entered Section 2 dosing. This trial is being performed in partnership with Sanofi, and is trying on the drug candidate as a remedy for lupus. Earlier this 12 months, Denali acquired a $15 million cost from Sanofi, in relation to the beginning of the Section 2 research. Denali has rights to additional milestone funds on this drug for improvement, regulatory, and gross sales progress, and can obtain royalties upon commercialization.

Lastly, in early September, Denali introduced that it had begun a Section 1b research of DNL343, a proposed remedy for ALS, or Lou Gehrig’s illness. This can be a extreme, progressive neurodegenerative illness, with a affected person base of 20,000 and as much as 5,000 new diagnoses annually within the US alone. The corporate plans to current wholesome volunteer knowledge on the DNL343 Section 1 research in October of this 12 months.

All of this offers Denali a number of pathways for future development – and introduced discover from Oppenheimer analyst Jay Olson.

“We view DNLI as an underappreciated rising chief in neurodegeneration and CNS problems with a number of late-stage improvement candidates primarily based on novel and differentiated mechanisms of motion (MOA) with sturdy preclinical and scientific knowledge. DNLI applies scientific insights into the genetic and organic processes underlying illness pathology to pursue biomarker methods that optimize improvement and potential industrial uptake,” Olson wrote.

The analyst added, “We view DNLI’s biomarker-driven strategy as de-risking improvement and commercialization primarily based on scientific rationale, and we consider that partnerships with trade leaders present exterior validation.”

Unsurprisingly, Olson charges this inventory an Outperform (i.e. Purchase) together with an $85 value goal. Traders stand to pocket ~67% achieve ought to the analyst’s thesis play out. (To look at Olson’s monitor document, click on right here)

General, DNLI has 10 analyst scores, break up amongst 7 Buys and three Holds. This provides the inventory a Average Purchase from the analyst consensus. Shares are promoting for $51, and the $91.38 common value goal suggests it has a 79% one-year upside potential. (See DNLI inventory evaluation at TipRanks.)

EZCORP, Inc. (EZPW)

The final Oppenheimer decide we’re is EZCORP, a Texas-based firm that operates pawn outlets throughout the US and Mexico, and into Central America. The corporate has a complete of 1,143 pawn retailer places, with 627 of that whole in Latin America.

On September 6, the corporate introduced that it had acquired 128 new shops in Mexico – these numbers are included within the totals above – for a purchase order value of $33.8 million. That value contains $17.3 million in money, 212,870 shares of EZPW frequent inventory, and compensation of $14.9 million price of the vendor’s debt. The vendor, Money Apoyo Efectivo, is entitled to further funds as much as $4.6 million within the subsequent two years primarily based on retailer efficiency. The newly acquired shops are positioned within the Mexico Metropolis space and have stable model recognition of their dwelling market.

The pawn enterprise thrives when persons are going through tough instances, and EZCORP’s shares replicate that. The inventory has gained 60% this 12 months, simply outpacing the S&P 500’s 19% achieve in the identical interval. Turning to monetary outcomes, EZCORP reported $174 million in whole income for its third fiscal quarter of 2021 (ending June 30), together with $157.2 million in excellent pawn loans. The pawn mortgage excellent quantity – a key metric for the corporate – was up 39% year-over-year. The corporate reported an enchancment in stock turnover from 2.9x to three.1x.

Brian Nagel, certainly one of Oppenheimer’s 5-star analysts, describes this firm as ‘ignored alternative,’ and writes: “Upon our preliminary research, we conclude that the corporate and its shares embody many key traits of finally profitable small-cap shopper funding tales, together with: 1) significant market share alternative inside a big and fragmented sector; 2) new senior management working to develop an improved technique and to strengthen company controls; 3) stable money place and steadiness sheet; 4) constructing exterior tailwinds enabling the corporate to raised leverage latest inside efforts; and 5) depressed fairness valuation.”

Taking the entire above into consideration, Nagel charges EZPW an Outperform (i.e. Purchase) together with a $12 value goal. This goal conveys his confidence in EZPW’s means to climb 57% greater within the subsequent 12 months. (To look at Nagel’s monitor document, click on right here)

Some shares slip beneath the radar, choosing up few analyst critiques regardless of sound efficiency, and that is one. Nagel’s is the one latest analyst assessment on document right here. (See EZPW inventory evaluation on TipRanks)

To search out good concepts for shares buying and selling at enticing valuations, go to TipRanks’ Greatest Shares to Purchase, a newly launched instrument that unites all of TipRanks’ fairness insights.

Disclaimer: The opinions expressed on this article are solely these of the featured analysts. The content material is meant for use for informational functions solely. It is extremely necessary to do your individual evaluation earlier than making any funding.

[ad_2]

Source link