[ad_1]

Over the previous few years, the growing success of the Money App has been Sq.’s (SQ) greatest development driver. This was very true in the course of the pandemic when the peer-to-peer providing grew at a speedy tempo on the peak of the stimulus packages. Whereas previous to the pandemic Money App revenue development exhibited a ~100% year-over-year uptick, this elevated to 276% YoY in July 2020, after which moderated to ~180% YoY in Aug/Sep.

Accordingly, when Sq. reviews 3Q21 earnings right this moment after the shut, Deutsche Financial institution’s Brian Keane expects the expansion to decelerate to 39% year-over-year, which can also be a drop from ~94% in 2Q21 as “fading stimulus advantages and tough comps,” come into play.

That mentioned, Keane thinks Sq. has sufficient firepower to mitigate towards the expansion deceleration of its star characteristic.

For one, the comps gained’t be fairly as robust when This fall comes round, leaving “potential” for year-over-year development to enhance barely into This fall.

Secondly, in distinction to the Money App, Sq.’s Vendor phase suffered in the course of the pandemic, and Keane is anticipating “robust transaction-based income development pushed by simpler comps and power on-line in addition to in-store.”

The analyst anticipates Vendor gross revenue to extend by roughly 50% year-over-year with “robust upside potential” to ~56%. This quantities to ~26% development on the 2-year timeframe, a rise on the ~21% development delivered in 2Q21.

Lastly, with Vendor “carrying upside” and the Money App anticipated to begin exhibiting indicators of a rebound on a year-over-year foundation in 4Q21, Keane expects consideration will flip to the “vital future synergies within the Afterpay deal.” Assuming the deal to convey the Australian purchase now, play later firm closes firstly of subsequent 12 months, these synergies might result in as a lot as $230 million of “incremental gross revenue” in FY22, which by FY23 might enhance to $1 billion.

“Importantly” the analyst summed up, “The deal additional connects the Vendor and Money App ecosystems growing the rate of fee flows.”

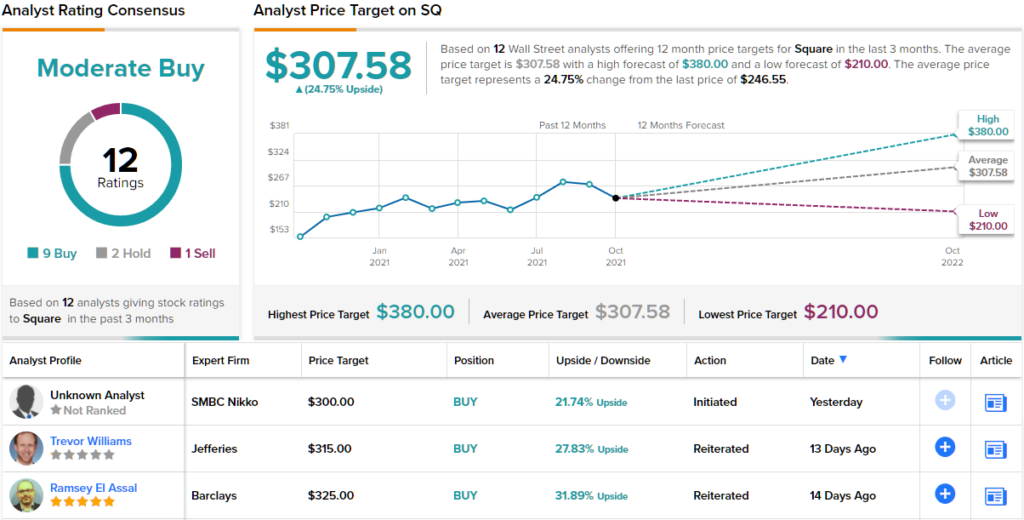

Nice information for Sq., then, however what are the implications for buyers? Keane reiterated a Purchase score together with a $330 worth goal, implying shares will add 34% of muscle over the approaching months. (To look at Keane’s observe document, click on right here)

Based on the remainder of the Avenue, there’s first rate upside within the playing cards, too; going by the $309.41 common goal, shares will respect by 21% within the 12 months forward. At the moment, the inventory boasts a Reasonable Purchase consensus score, based mostly on 13 Buys, 4 Holds and 1 Promote. (See Sq. inventory evaluation on TipRanks)

To search out good concepts for shares buying and selling at engaging valuations, go to TipRanks’ Finest Shares to Purchase, a newly launched software that unites all of TipRanks’ fairness insights.

[ad_2]

Source link