[ad_1]

Iran started the brand new fiscal yr on March 21, 2022 having recorded an estimated GDP development fee of about 4% over the earlier yr and three% for the non-oil sector. The patron worth index (CPI) has grown by 35% year-on-year, in line with the Statistical Heart of Iran (SCI). Whereas GDP development might be the results of the stabilization of the financial system after a number of years of recession on account of harsh sanctions and financial mismanagement, a gradual fee of excessive inflation is alarming for Iran’s financial system.

Over the previous decade, CPI has elevated by 735%, whereas the financial system has grown by solely 7.2%, in line with knowledge from the SCI. The Central Financial institution of Iran (CBI)1 places the determine even decrease, at simply 5.7%. Throughout the identical interval, regional friends Saudi Arabia, Iraq, and Turkey grew by 16.2%, 31.9%, and 48.8%, respectively, whereas their CPI rose by 115%, 114%, and 248%, in line with knowledge from the World Financial institution. Iran’s divergent efficiency is the results of numerous sanction regimes imposed by the worldwide group in 2011-15 and by the U.S. since 2018. Additionally it is the results of poor fiscal self-discipline brought on by the dysfunctional nature of Iran’s political financial system, which permits for the complete interdependence of the CBI and the federal government.2

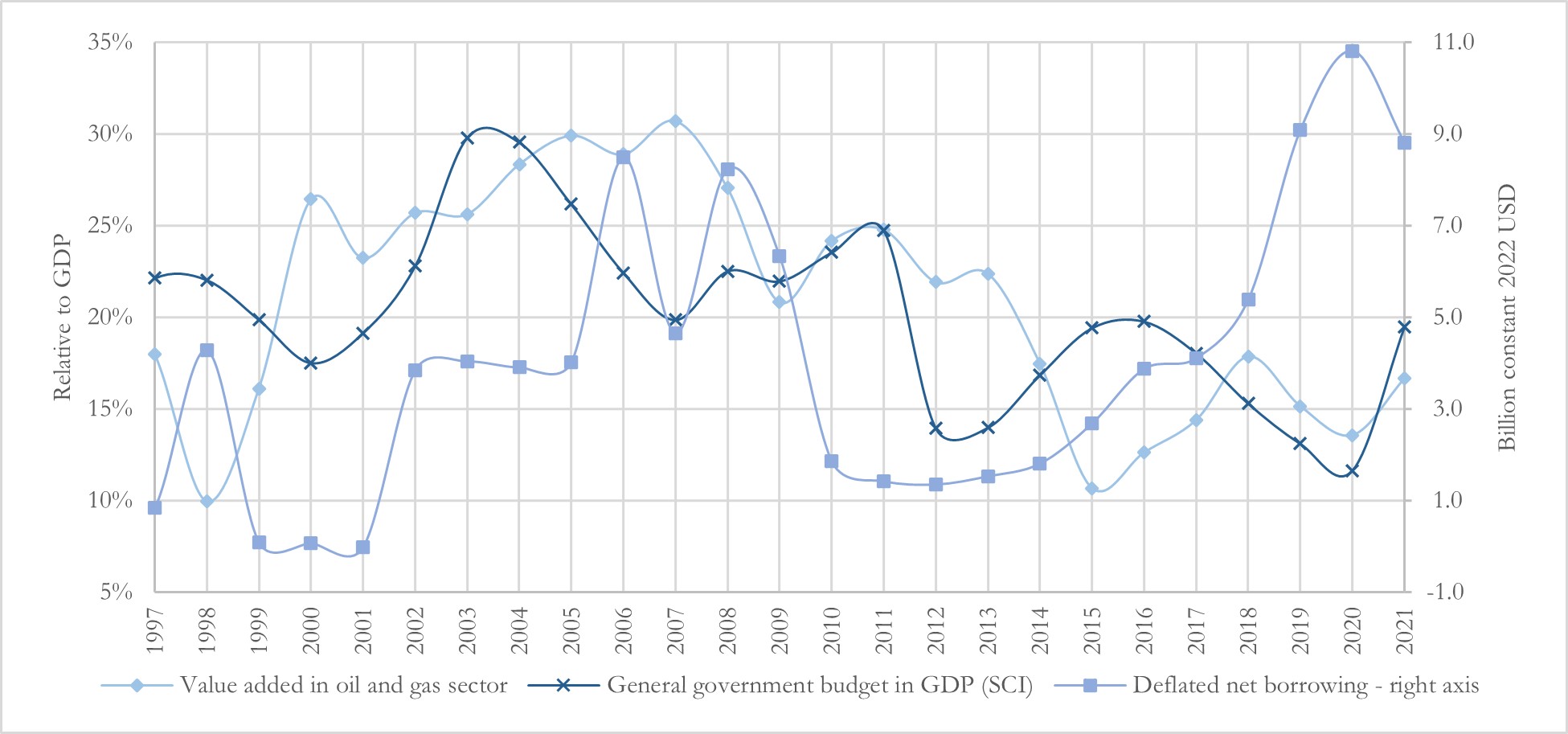

Determine 1: Growth of oil and gasoline sector, normal authorities funds, and web authorities borrowing, 1997-2021

Be aware: Nominal GDP is used from SCI to calculate shares in GDP; GDP deflator is used from CBI to deflate web borrowing; estimated values by creator are used for yr 2021 (i.e., the fiscal yr beginning on March 21, 2021); every USD is the same as IRR 278,000 for the calculation of borrowing on the appropriate vertical axis.

The pure useful resource curse

Oil revenues have lengthy been the federal government’s essential supply of revenue. On the oil worth peak in 2008, oil contributed 30.7% of Iran’s GDP (see Determine 1). After the worldwide group intensified sanctions, the share of oil in Iran’s GDP fell considerably, dropping to only 10.6% in 2015. As Determine 1 illustrates, the overall authorities funds relative to GDP through the interval 1997-2020 has tended to maneuver in lockstep with oil’s share of GDP, however fluctuations have usually been of a smaller magnitude.

When oil revenues fell in need of the federal government funds, the federal government sought various sources of income. These are poorly developed and onerous to seek out given the scale of the tax-exempt public financial system, that means the federal government has usually needed to flip to borrowing as a final resort. Choices at its disposal embody borrowing from the banking system by issuing Islamic bonds, from the Nationwide Growth Fund of Iran, from the CBI by printing cash, and from the sale of presidency property by means of casual channels and the Tehran Inventory Trade. These mechanisms have normally contributed to a considerable improve within the financial base on account of limitations on Iran’s monetary and capital markets, that are lower off from the worldwide financial system.

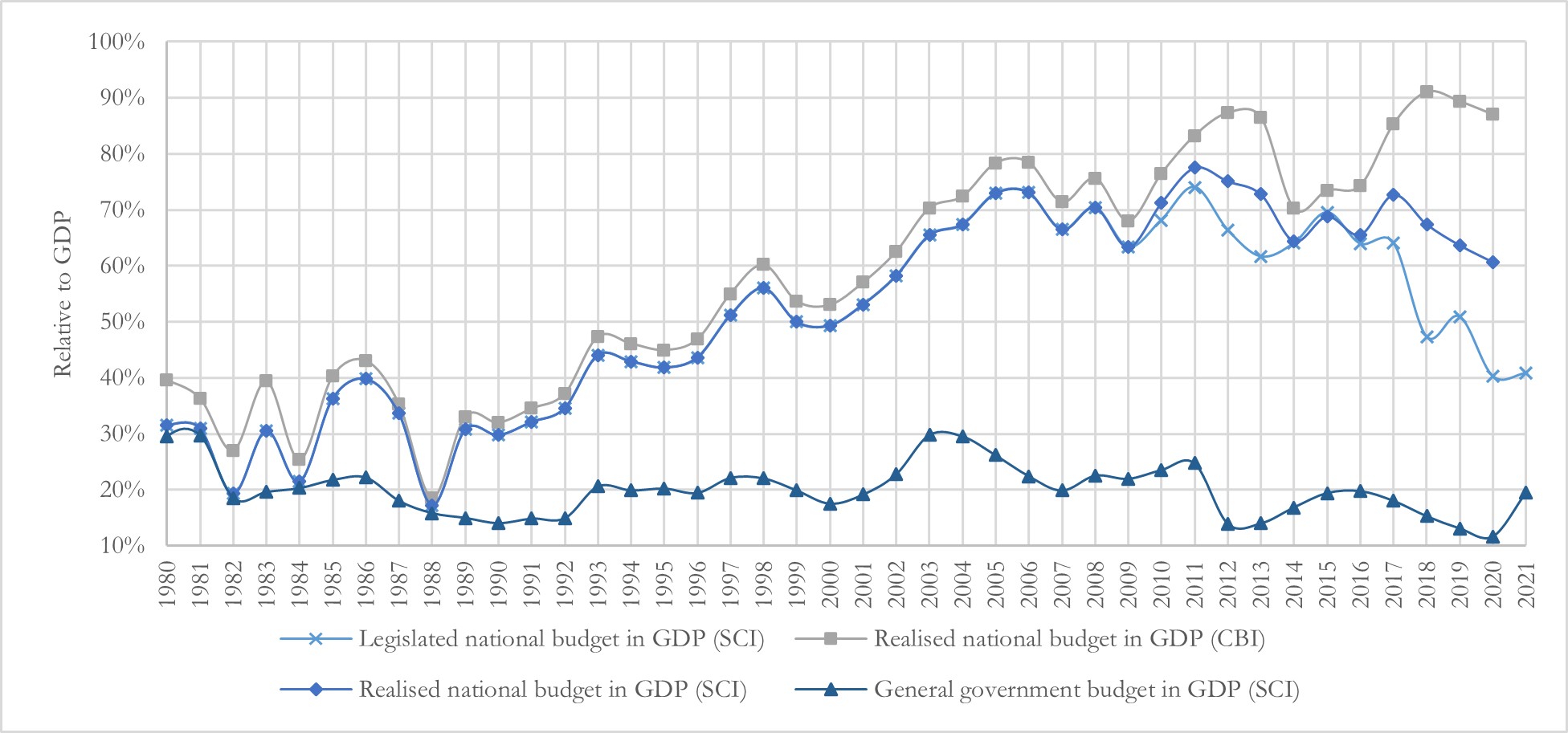

Determine 2: Growth of complete nationwide funds, and normal authorities funds as shares of GDP in Iran, 1980-2021

Be aware 1: for the years 2010 onwards, the info on realized nationwide funds from SAC experiences are used.

Be aware 2: dimension of the general public enterprise is the space between the overall nationwide funds and the overall authorities funds.

Be aware 3: estimated values by creator are used for yr 2021 (i.e., the fiscal yr beginning on March 21, 2021).

Though in previous years oil revenues exceeded the overall authorities funds, Iran allotted a part of the funds to repay earlier debt at maturity. However when oil revenues are so low that they can not cowl the matured debt, the quantity of borrowing exceeds the earlier debt reimbursement. Solely in 1999-2001 beneath President Mohammad Khatami was the federal government’s web borrowing adverse (see Determine 1), that means a part of the federal government debt was being paid off with out creating new debt. In all different years, governments have been borrowing greater than they had been repaying. Fiscal self-discipline was at its worst in actual phrases in 2006-09 beneath President Mahmoud Ahmadinejad, regardless of the height in oil revenues, and through President Hassan Rouhani’s second time period (2017-21), particularly because the U.S. reimposed secondary sanctions in 2018.

An excessively massive public financial system and a rising public debt

Earlier than each fiscal yr, the federal government submits the nationwide funds invoice to parliament for legislating. In accordance with the Supreme Audit Court docket (SAC), nevertheless, the overall funds of public enterprises — i.e., all publicly owned firms, banks, and establishments — has been a lot bigger than that legislated lately (see Determine 2). In accordance with annual experiences by SAC, over the previous 4 a long time, the overall nationwide funds, together with each the overall authorities funds and that of public enterprises, has elevated from 40% of GDP (per CBI figures) in 1980 to 91% in 2018. In accordance with nominal GDP figures from the SCI,3 the relative dimension of the nationwide funds reached a peak of 78% in 2011 earlier than the worldwide group ramped up sanctions. each sources, it’s clear that almost all of Iran’s financial system is managed by the general public sector and solely a small portion is managed by the personal sector and semi-public enterprises.

Furthermore, authorities borrowing lately has led to the buildup of each authorities and public debt. In accordance with a report from parliament, the overall debt of public enterprises on the finish of FY2020-21 stands at IRR 9,100 trillion ($32.7 billion), equal to 37% of the funds and 26% of Iran’s GDP that yr (per CBI). The amassed debt of the overall authorities in the identical yr is the same as IRR 6,900 trillion ($24.8 billion) — 118% of the funds and 24.8% of GDP that yr (per CBI). Which means that the overall amassed debt of the general public financial system with out semi-public firms stood at 45.6% of GDP in March 2021.

Paying again debt and financing the funds is the only greatest problem for Iran’s financial system. Sadly, the Raisi authorities believes borrowing and issuing new authorities bonds is a extra sustainable approach of doing this than having the CBI print cash. Persistent accumulation of debt, nevertheless, is unsustainable, as a result of it results in monetization of fiscal coverage, whereby outdated debt is paid off by new debt, fairly than tax income. In accordance with knowledge from the IMF, in Venezuela the persistent monetization of fiscal coverage resulted in large year-on-year inflation of 130,000% in 2018 and gross public debt that just about doubled in simply three years, rising from 180% of GDP in 2018 to 330% in 2021. As debt shrinks in actual phrases over time with excessive inflation, one might argue that policymakers in Iran are deliberately pursuing monetization and excessive inflation.

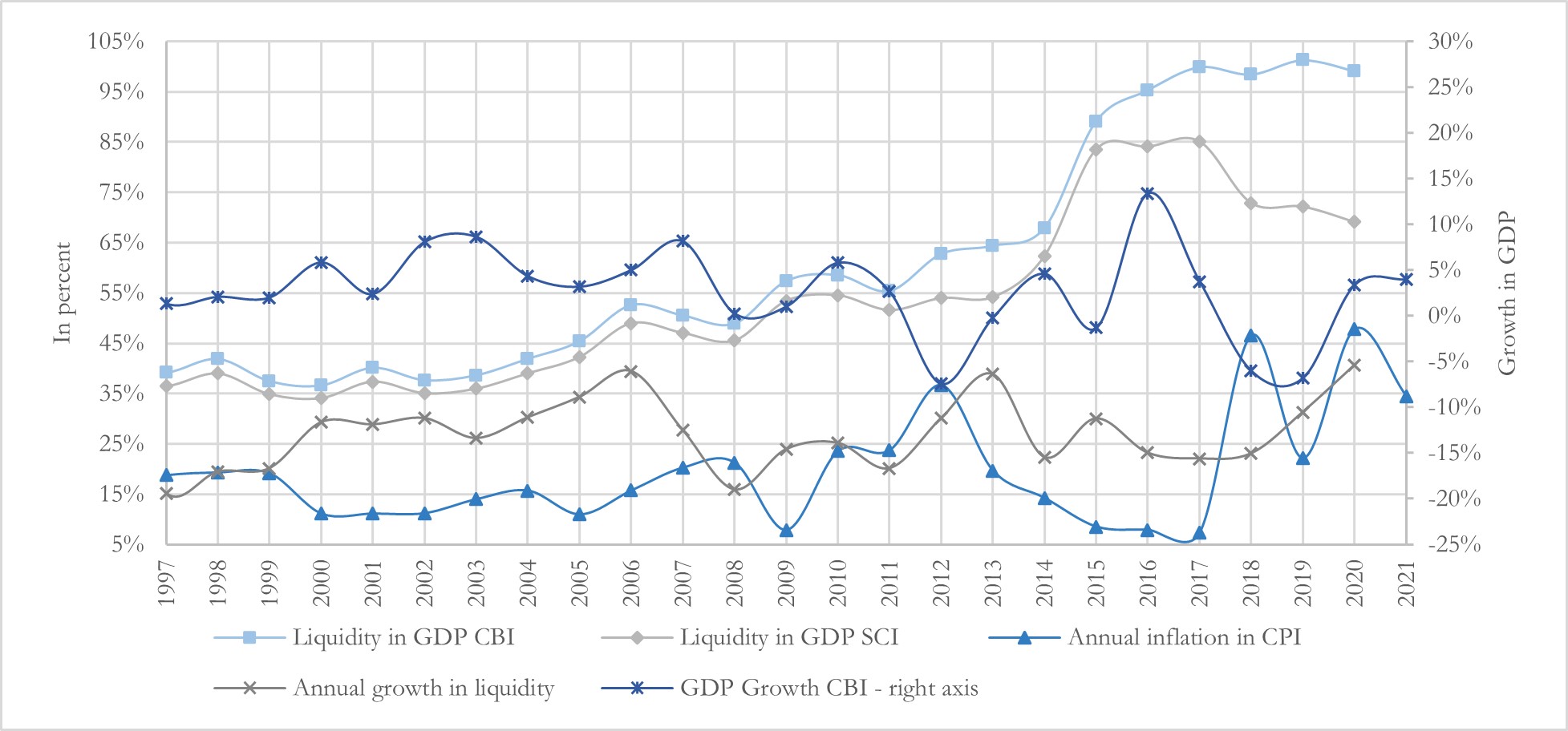

Determine 3: Growth of financial indicators and GDP development, 1997-2021

Be aware 3: estimated values by creator are used for yr 2021 (i.e., the fiscal yr beginning on March 21, 2021).

Borrowing has grow to be the most important supply of financing funds deficits

As defined above, borrowing has drawn on a number of sources, all of which have elevated the financial base and liquidity. Liquidity relative to GDP (per CBI) has been on the rise. But some experts4 near the federal government have famous that the ratio of liquidity to GDP (per SCI) was very excessive throughout 2015-17 whereas inflation was very low, and since then the ratio has decreased whereas inflation has elevated. Based mostly on this, they argue that liquidity has no affect on inflation. They’ve additionally advocated for the federal government to rely extra on the financial base each time wanted. This brings them to a conclusion that may hinder efforts in parliament to implement structural reforms to facilitate the CBI’s independence from the federal government. In accordance with any commonplace macroeconomics textbook, nevertheless, development of liquidity and the financial base results in rising costs whereas conserving GDP development and velocity of cash fixed. Throughout 2015-17, the expansion in liquidity fell in need of that of GDP (see Determine 3), resulting in low CPI development.5

Moreover, these similar specialists argue that top inflation is solely the results of growing import costs because the alternate fee depreciates or the worth of overseas items will increase. On this foundation, they’re advocating for a set alternate fee. Typical knowledge has it that greater import costs result in greater inflation, relying on their contribution to combination demand and the way “upstream” the imported items are — i.e., the space from manufacturing to consumption. In 2018 the preliminary worth hikes had been as a result of depreciation of the rial and growing imported commodity costs. The value hikes now for wheat and wheat merchandise are as a result of elimination of the low preferential alternate fee on the remaining imported main items. Nonetheless, one can not underestimate the affect of development in cash on development in costs within the years after the alternate fee was comparatively stabilized. Furthermore, a rustic can not implement an autonomous financial coverage with a set alternate fee regime when rate of interest parity holds. With a set alternate fee regime, Iran must impose capital controls and isolate its capital and monetary markets from the worldwide financial system to keep up an autonomous financial coverage. This appears to be the true goal of the specialists advocating these insurance policies.

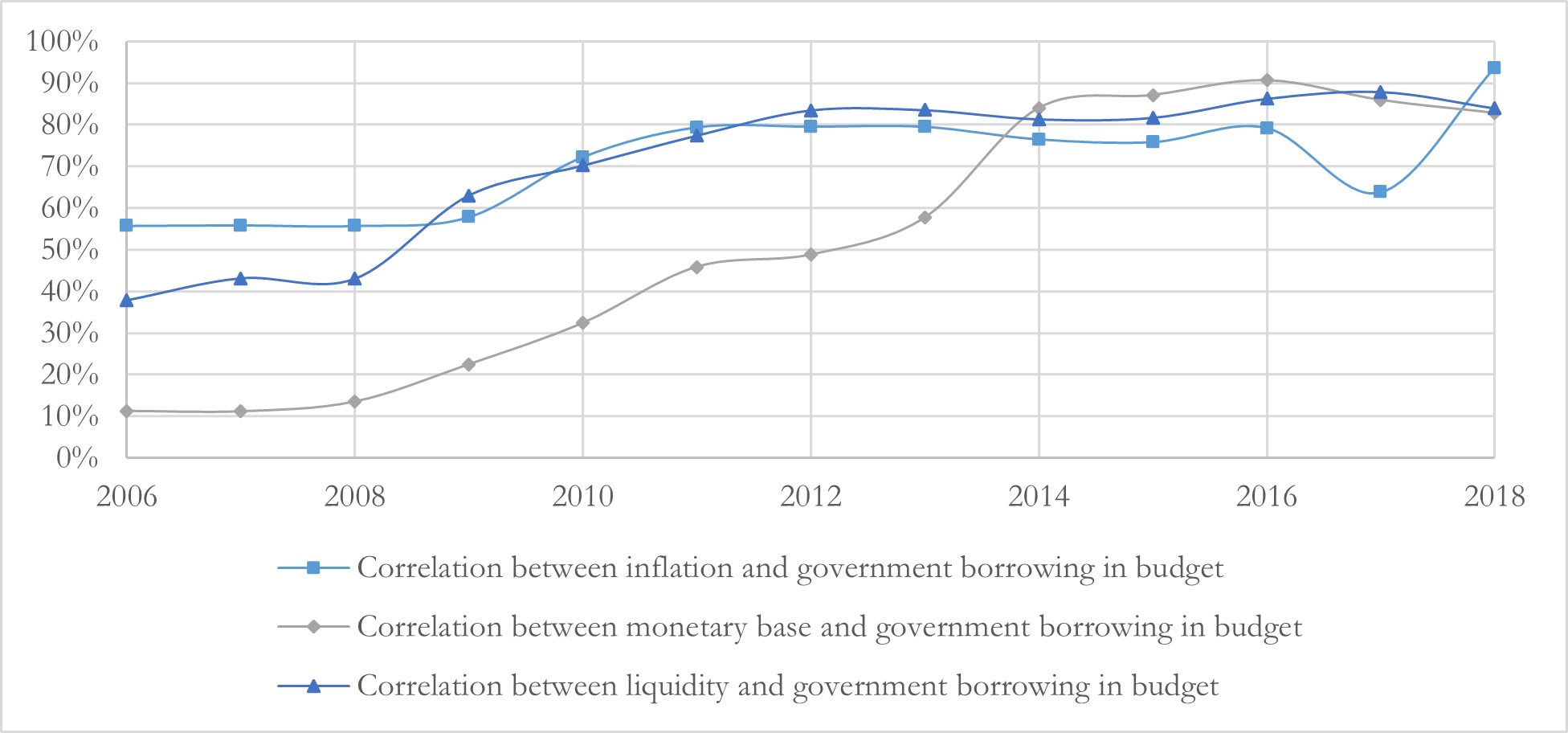

Determine 4: Correlation between authorities web borrowing and financial indicators, 2006-2018

By advocating expansionary financial coverage when the federal government funds wants it, specialists near the highest establishments are attempting to consolidate the monetization of fiscal coverage, which has not proven optimistic ends in Iran or every other nation. The correlation between the federal government’s web borrowing relative to funds and development in financial base, liquidity, and costs has elevated considerably lately (see Determine 4), which units off alarm bells concerning the monetization of fiscal coverage in Iran. These specialists are both advocating this without having full foresight of the results, or they know precisely what they’re doing and wish to convey a few disaster.6

What are the very best coverage choices for Raisi?

To keep away from a disaster, the Raisi authorities should first perceive the issue earlier than it will get worse. The federal government mustn’t resort to decreasing the overall authorities funds by chopping actual wages as these specialists have advocated. Within the present funds invoice, the Raisi authorities solely included a ten% elevate for public workers and pensioners — far beneath inflation. Given the scale of the general public financial system, this may have an effect on the biggest a part of the employed inhabitants, inflicting widespread discontent and doubtlessly sparking fierce protests. The Raisi authorities, nevertheless, could also be ready to suppress these.

Second, Raisi should additionally perceive that overhauling Iran’s financial system would require selling the personal sector and decreasing the scale of the general public financial system, which since 1980 has been steadily swallowing the broader financial system. A failed privatization drive through the Ahmadinejad administration solely empowered the semi-public sector, leading to weaker improvement of productiveness, expertise, and worldwide competitiveness whereas growing political lease and corruption. For Iran to grow to be a stronger regional or worldwide energy, it first must overhaul its financial system. To take action, very similar to the Soviet Union, it should transfer away from central planning and undertake a extra liberal financial system with the frequent imposition of acceptable laws to regulate for adverse externalities of the market. This can require main structural reforms within the political system and the financial system to draw personal and overseas direct funding.

Iranians now really feel the ache of sanctions and blame the ruling elite for making poor coverage decisions that introduced them financial distress. Though eradicating sanctions and boundaries to commerce is standard knowledge within the trendy financial system and an important aim for Iran, the negotiations in Vienna on which this hinges proceed to be hampered by political motives that aren’t associated to the principle situation beneath dialogue, Iran’s nuclear program. Oblique negotiations between the U.S. and Iran are at a standstill. This comes as Iran has been capable of export extra oil to China because the Biden administration informally allowed it, easing the financial strain on the brand new authorities, which has additionally benefited from greater oil costs. This won’t be sustainable, nevertheless, if the negotiations fail and the U.S. doubles down on sanctions. With the present surge in oil costs following the Russian invasion of Ukraine, Iran should seize the chance to safe a deal on the nuclear situation that may assist facilitate the restoration of its financial system, after which construct on this by means of step-by-step negotiations to deal with the remaining problems with concern.

Dr. Mahdi Ghodsi is an economist on the Vienna Institute for Worldwide Financial Research and an Adjunct Professor at Vienna College of Economics and Enterprise. His analysis focuses on worldwide commerce, worldwide commerce coverage, non-tariff measures, industrial coverage, overseas direct funding, international worth chains, political financial system of sanctions, and the Iranian financial system. You’ll be able to comply with him on Twitter. The views expressed on this piece are his personal.

Photograph by Morteza Nikoubazl/NurPhoto by way of Getty Pictures

Endnotes

- This paper additionally highlights the significance of the big distinction between the statistics offered by the 2 public establishments, which can additionally end in totally different insurance policies and goals.

- It’s price noting that the lack of confidence within the independence of the Central Financial institution of the Republic of Turkey (CBRT) because of the gradual accumulation of energy by President Recep Tayyip Erdoğan has additionally precipitated annual inflation to surge to over 70% and substantial depreciation of the Turkish Lira.

- Nominal GDP in 2020 (i.e., the fiscal yr beginning on March 21, 2020) offered by SCI is 43% bigger than that offered by the CBI.

- These specialists are a part of the younger revolutionaries and Hezbollahi elites advising the principle establishments of the Islamic Republic, such because the Expediency Discernment Council or the Islamic Revolutionary Guard Corps. The necessity for Iran to develop a “resistance financial system” that’s utterly self-sufficiency in items and providers is their essential financial concept. They’re principally political science graduates however are advising on financial points in opposition to the theories of economics as they consider these theories have introduced liberalism and neo-liberalism and are in opposition to Iran’s pursuits.

- That is referred to the Amount Concept of Cash: cash provide (M) × velocity of cash (V) = worth stage (P) × actual GDP (Q). And it’s assumed that the speed of cash stays comparatively fixed within the brief run because it will depend on institutional components such because the frequency of wage funds inside every year. Which means that when development in M will increase, and Q stays fixed, P ought to improve as a lot as the expansion in M as the speed didn’t change after one interval.

- This might doubtlessly be associated to the re-emergence of the final Imam. See as an illustration, level 3a in https://www.al-islam.org/faith-and-reason/question-25-signs-re-emergence-imam-al-mahdi_.

[ad_2]

Source link

%20who%20is%20visiting%20the%20Agency%20on%20the%2075th%20anniversary%20of%20its%20founding%20in%20Langley,%20Virginia,%20on%20July%208,%202022%20-%20AFP.jpg?itok=IqZpGQ2M)

{kind=link}