[ad_1]

The previous couple of months, except for some brief bullish buying and selling runs, have been brutal for the markets. Shares are down, just about throughout the board. The tech-heavy NASDAQ index has fallen 25% year-to-date, whereas the broader S&P 500 is down 16%.

As for causes to the market turndown, you may take your choose. Provide chains stay snarled, and the Chinese language authorities’s anti-COVID lockdown insurance policies and the Russian battle in opposition to Ukraine aren’t serving to that matter any. Inflation, which began taking off a yr in the past, stays stubbornly excessive, at ranges not seen in 40 years or extra. And whereas the job market continues to point out positive factors, the economic system continues to be brief greater than 1,000,000 jobs from pre-pandemic ranges.

So it’s a tricky macro-economic image, one which makes it ever tougher for buyers to know simply what strikes to make. It’s time to discover a sign, some signal that may present simply what shares are prone to carry returns going ahead.

That is the place the Insiders’ Sizzling Shares device at TipRanks can make clear issues. By monitoring the buying and selling exercise of company officers, the insiders, buyers can see what shares getting snapped up by ‘these within the know,’ and might comply with their lead. We’ve gotten that course of began, pulling up the main points on two beaten-down shares which have each proven some main insider shopping for. Let’s take a better look.

iMedia Manufacturers (IMBI)

First up is iMedia Manufacturers, a pacesetter within the interactive media world with a portfolio of property together with a powerful presence within the area of interest of TV-shopping universe. iMedia’s channels embrace ShopHQ and ShopHQ Well being, ShopBulldogTV, and ShopLaventa, together with such digital property because the end-to-end OTT streaming service Float left, and the digital logistics service i3PL. Final fall, iMedia closed its newest acquisition, of 123tv, the German tv retail market, in a deal price $93 million, together with a $72 million money fee.

iMedia shall be presenting its 1Q22 numbers later this month, however in a preliminary launch administration stated it expects a prime line between $154 million and $157 million. This might characterize year-over-year income progress within the vary of 35% to 38%, and could be according to the beforehand revealed steering of $156 million. The corporate expects its web loss to deepen, from $3.3 million within the year-ago quarter to the vary $11.9 million to $12.3 million within the coming report. Waiting for the total yr 2022, the corporate is guiding towards whole revenues of $675 million to $725 million, or y/y prime line progress of 23% to 32%. Assembly this preliminary report will give iMedia 4 consecutive quarters with sequential income positive factors.

iMedia introduced on Could 12 the pricing of a brand new sale of inventory, to boost about $24 million. The inventory dilution pushed the shares all the way down to 52-week low.

The insiders, nevertheless, usually are not so apprehensive. 4 members of the corporate’s board made ‘informative buys’ at the moment. Two of these buys had been for $100K or much less; the third was for $600,000. The fourth purchase, nevertheless, made by director Eyal Lalo, was much more substantial. Lalo picked up 390,880 shares, placing down $1.2 million for the inventory.

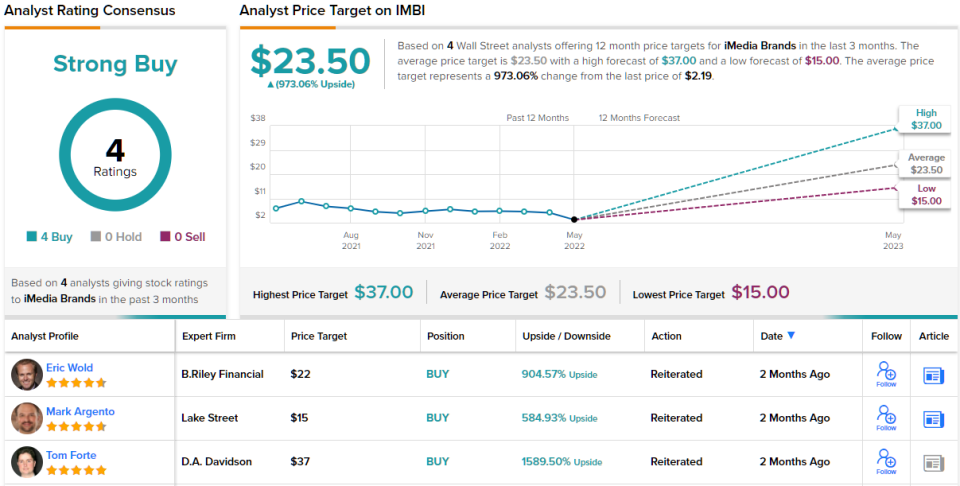

Masking iMedia for Craig-Hallum, analyst Alex Fuhrman reminds buyers that there are sturdy positive factors in retailer for IMBI. Fuhrman charges the inventory a Purchase, and his $20 worth goal implies an upside of an enormous 813% on the one-year time horizon. (To look at Furhman’s observe document, click on right here)

“We’re inspired that the corporate is ready to reiterate its outlook regardless of volatility stemming from Russia’s invasion of Ukraine, particularly contemplating that IMBI generates greater than 20% of its revenues in Germany, Poland, and Austria by way of its 2021 acquisition of German TV retailer 123tv. The sturdy vacation season outcomes are much more spectacular when you think about that the majority massive e-commerce firms not named Amazon (e.g. 1-800 Flowers, QVC, HSN) reported lower-than-expected outcomes for This autumn as rising freight and labor prices have eroded margins,” Fuhrman wrote.

Total, all 4 of the current analyst critiques on this inventory are in settlement with the bullish outlook, giving the inventory its unanimous Sturdy Purchase consensus ranking. The shares are priced at simply $2.19 and their $23.50 common worth goal suggests a extremely sturdy upside of 973% within the subsequent 12 months. (See IMBI inventory forecast on TipRanks)

Corsair Gaming (CRSR)

Let’s change gears a bit, and try Corsair Gaming. That is one other tech firm, however one which works on the {hardware} aspect. Corsair develops, manufactures, and markets the high-end gear that PC players like to have. Amongst Corsair’s product line are streaming gear, headsets, sensible ambient lighting, audio methods, and displays – the peripherals that improve the gaming expertise are beloved by players from creators to hobbyists to critical gamers. Corsair additionally provides energy provide items, stable state drives, reminiscence chips, and case coolers.

Corsair has had a tough time in current months, because the PC gaming sector hasn’t seen as massive a rebound because the extra conventional brick-and-mortar economic system. The explanations are manifold, and complicated. Whereas shopper spending is up, spending on video games has dropped again after the preliminary post-lockdown bounce. The {hardware} and peripherals are topic to each manufacturing and provide line delays, elements which had been exacerbated by the lockdowns in China and the battle in Ukraine. So it might be no marvel that CRSR shares have misplaced 50% within the final 12 months.

On the similar time, the monetary outcomes Corsair reported earlier this month, for 1Q22, had been in-line with the beforehand revealed steering. Corsair reported a prime line of $380.7 million, down 28% from 1Q21, and displays the year-ago quarter’s pent-up demand and the increase from authorities COVID stimulus checks. It is very important be aware that the 1Q22 income was up 23% from the pre-pandemic 1Q20.

On the insider entrance, Board member Samuel Szteinbaum final week made a hefty buy of firm inventory. His purchase totaled 80,000 shares and value greater than $1.14 million. That inventory purchase bumped his holding within the firm to a price of $3.63 million.

Corsair inventory is roofed by D.A. Davidson analyst Franco Granda, who notes the headwinds which might be pushing the gaming business round lately, however nonetheless comes down on an optimistic be aware.

“Though CRSR has finished an excellent job at sourcing merchandise to fulfill demand, business headwinds are proving tough to beat for everyone. If a damaged provide chain and inflation weren’t sufficient, COVID lockdowns in China and the Ukraine battle are exacerbating the NT enterprise. 70% of the Y/Y declines in 1Q22 originated from Europe, highlighting the influence of diminished shopper confidence, significantly following the beginning of the battle… Regardless of these pressures, the corporate continues to achieve share (innovation and product availability) within the areas it’s a chief in. In reality, CRSR already exceeded its goal to achieve 1% share yearly, in 1Q alon,” Granda opined.

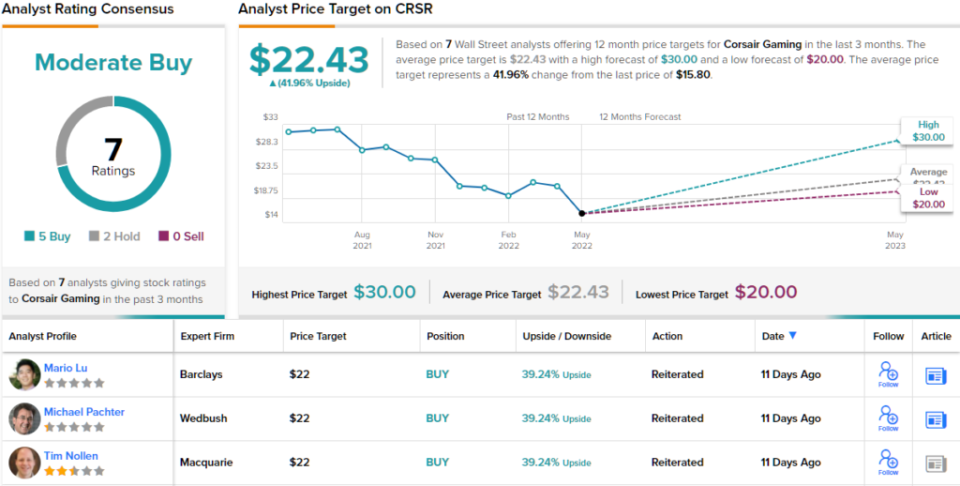

In step with this outlook, Granda charges CRSR shares a Purchase, with a $28 worth goal to suggest a 77% upside for the yr forward. (To look at Granda’s observe document, click on right here)

Total, the sentiment on the Road would agree with the bulls on this gaming firm. Corsair has 7 current critiques, which break down 5 to 2 in favor of Buys over Holds and assist the Average Purchase consensus ranking. Shares have a mean worth goal of $22.43, suggesting ~42% upside from the buying and selling worth of $15.80. (See CRSR inventory forecast on TipRanks)

To seek out good concepts for shares buying and selling at engaging valuations, go to TipRanks’ Finest Shares to Purchase, a newly launched device that unites all of TipRanks’ fairness insights.

Disclaimer: The opinions expressed on this article are solely these of the featured analysts. The content material is meant for use for informational functions solely. It is extremely essential to do your individual evaluation earlier than making any funding.

[ad_2]

Source link