[ad_1]

The oil market is at present going by way of one of the crucial turbulent durations because the notorious March 2020 collapse, as traders proceed to grapple with recessionary fears. Oil costs have continued sliding within the wake of the central financial institution deciding to hike the rate of interest by a record-high 75 foundation factors, with WTI futures for July settlement had been quoted at $104.48/barrel on Wednesday’s intraday session, down 4.8% on the day and eight.8% under final week’s peak. In the meantime, Brent crude futures for August settlement had been buying and selling 4% decrease in Wednesday’s session at $110.10/barrel, a superb 9.4% under final week’s peak.

Whereas crude costs have taken a giant hit, oil and gasoline shares have fared even worse, with vitality equities experiencing almost double the promoting strain in comparison with WTI crude.

“12 months so far, Power is the only real sector within the inexperienced … however concern now could be that incontrovertible fact that Bears are coming after winners, thus they might take Power down. The Power Sector undercut its rising 50 DMA and now seems to be decrease to the rising 200 DMA, which is at present -9% under final Friday’s shut. Crude Oil is sitting on its rising 50 DMA and has a stronger technical sample,” MKM Chief Market Technician J.C. O’Hara has written in a be aware to purchasers.

“Usually we like to purchase pullbacks inside uptrends. Our concern at this level within the Bear market cycle is that management shares are sometimes the final domino to fall, and thus revenue taking is the larger motivation. The fight-or-flight mentality at present favors flight, so we’d relatively downsize our positioning in Power shares and harvest among the outsized good points achieved following the March 2020 COVID low,” he has added.

Associated: Russian Refinery On Fireplace After Kamikaze Drone Strike

In keeping with O’Hara’s chart evaluation, these vitality shares have the best draw back danger:

Antero Midstream (NYSE:AM), Archrock (NYSE:AROC), Baker Hughes (NASDAQ:BKR), DMC International (NASDAQ:BOOM), ChampionX (NASDAQ:CHX), Core Labs (NYSE:CLB), ConocoPhillips (NYSE:COP), Callon Petroleum (NYSE:CPE), Chevron (NYSE:CVX), Dril-Quip (NYSE:DRQ), Devon Power (NYSE:DVN), EOG Sources (NYSE:EOG), Equitrans Midstream (NYSE:ETRN), Diamondback Power (NASDAQ:FANG), Inexperienced Plains (NASDAQ:GPRE), Halliburton (NYSE:HAL), Helix Power (NYSE:HLX), World Gasoline Companies (NYSE:INT), Kinder Morgan (NYSE:KMI), NOV (NYSE:NOV), Oceaneering Worldwide (NYSE:OII), Oil States Worldwide (NYSE:OIS), ONEOK (NYSE:OKE), ProPetro (NYSE:PUMP), Pioneer Pure Sources (NYSE:PXD), RPC (NYSE:RES), REX American Sources (NYSE:REX), Schlumberger (NYSE:SLB), U.S Silica (NYSE:SLCA), Bristow Group (NYSE:VTOL), and The Williams Firms (NYSE:WMB).

Tight Provides

Whereas the bear camp, together with the likes of O’Hara, believes that the oil value rally is over, the bulls have stood their floor and consider the most recent selloff as a brief blip.

In a latest interview, Michael O’Brien, Head of Core Canadian Equities at TD Asset Administration, informed TD Wealth’s Kim Parlee that the oil provide/demand fundamentals stay rock stable thanks largely to years of underinvestment each by non-public producers and NOCs.

You’ll be able to blame ESG—in addition to expectations for a lower-for-longer oil value surroundings over the previous couple of years—for taking a toll on the capital spending of exploration and manufacturing (E&P) firms. Certainly, precise and introduced capex cuts have fallen under the minimal required ranges to offset depletion, not to mention meet any anticipated progress. Oil and gasoline spending fell off a cliff from its peak in 2014, with international spending by exploration and manufacturing (E&P) corporations hitting a nadir in 2020 to a 13-year low of simply $450 billion.

Even with greater oil costs, vitality firms are solely rising capital spending steadily with the bulk preferring to return extra money to shareholders within the type of dividends and share buybacks. Others like BP Plc. (NYSE:BP) and Shell Plc. (NYSE:SHEL) have already dedicated to long-term manufacturing cuts and can battle to reverse their trajectories.

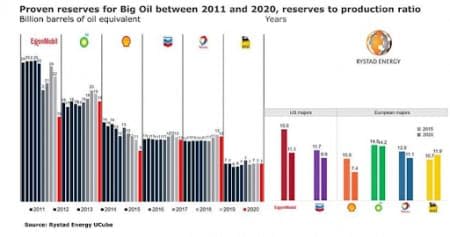

Norway-based vitality consultancy Rystad Power has warned that Large Oil might see its confirmed reserves run out in lower than 15 years, due to produced volumes not being absolutely changed with new discoveries.

In keeping with Rystad, confirmed oil and gasoline reserves by the so-called Large Oil firms specifically ExxonMobil (NYSE:XOM), BP Plc., Shell, Chevron (NYSE:CVX), TotalEnergies ( NYSE:TTE), and Eni S.p.A (NYSE:E) are all falling, as produced volumes usually are not being absolutely changed with new discoveries.

Supply: Oil and Fuel Journal

Large impairment costs has seen Large Oil’s confirmed reserves drop by 13 billion boe, good for ~15% of its inventory ranges within the floor. Rystad now says that the remaining reserves are set to expire in lower than 15 years, until Large Oil makes extra industrial discoveries rapidly.

The primary wrongdoer: Quickly shrinking exploration investments.

International oil and gasoline firms reduce their capex by a staggering 34% in 2020 in response to shrinking demand and traders rising cautious of persistently poor returns by the sector.

ExxonMobil, whose confirmed reserves shrank by 7 billion boe in 2020, or 30%, from 2019 ranges, was the worst hit after main reductions in Canadian oil sands and U.S. shale gasoline properties.

Shell, in the meantime, noticed its confirmed reserves fall by 20% to 9 billion boe final yr; Chevron misplaced 2 billion boe of confirmed reserves attributable to impairment costs, whereas BP misplaced 1 boe. Solely Whole and Eni have averted reductions in confirmed reserves over the previous decade.

The outcome? The U.S. shale trade has solely managed to bump up 2022 crude output by simply 800,000 b/d, whereas OPEC has persistently struggled to satisfy its targets. In actual fact, the scenario has change into so unhealthy for the 13 nations that make up the cartel that OPEC+ produced 2.695 million barrels per day under its crude oil targets within the month of Might.

Exxon CEO Darren Woods has predicted that the crude markets will stay tight for as much as 5 years, with time wanted for corporations to “catch up” on the investments wanted to make sure provide can meet demand.

“Provides will stay tight and proceed supporting excessive oil costs. The norm for ICE Brent continues to be across the $120/bbl mark,” PVM analyst Stephen Brennock has informed Reuters after the most recent crude selloff.

In different phrases, the oil value rally is likely to be removed from over, and the most recent correction would possibly supply recent entry factors for traders.

Credit score Suisse vitality analyst Manav Gupta has weighed in on the shares with essentially the most publicity to grease and gasoline costs. You could find them right here.

In the meantime, you could find among the least expensive oil and gasoline shares right here.

By Alex Kimani for Oilprice.com

Extra Prime Reads From Oilprice.com:

Learn this text on OilPrice.com

[ad_2]

Source link