[ad_1]

The outlook for the semiconductor sector is transferring from unhealthy to worse, and buyers look like transferring their cash into the software program sector in consequence.

Pessimism about the way forward for the chip sector has been rising after a blended spherical of forecasts within the second quarter, with analysts signaling that the pandemic-driven increase in gross sales amid provide issues might dry up. They worry that prospects overbought through the supply-chain frenzy, which might make them halt purchases as a result of they have already got stock, and are starting to see indicators that’s taking place.

Don’t miss: Why semiconductor shares are ‘virtually uninvestable’ regardless of document earnings amid a worldwide scarcity

Mizuho analyst Jordan Klein and Bernstein analyst Stacy Rasgon checked on this week with notes outlining their doubts that the increase in chip gross sales will proceed into subsequent 12 months.

“It feels worse that it has been throughout buy-side all 12 months,” Klein wrote in a be aware Friday. “Everybody tremendous unfavorable and cautious primarily based on checks out of Asia suggesting reminiscence pricing falling, smartphone and PC provide chains downticking as inventories rise and demand/orders gradual.”

“Whereas information middle/server and auto provide chains sound good, few appear to need to purchase/add to those semi shares fearing weak point elsewhere will harm all semi sentiment and valuations,” Klein stated. “And if cloud capex spend will get lower, it might be recreation over for a number of the favored and owned semi names like Marvell Expertise Inc.

MRVL,

Superior Micro Gadgets Inc.

AMD,

Nvidia Corp.

NVDA,

that concentrate on the information middle.”

Rasgon wrote on Tuesday that “it looks like buyers are ready for any individual to blink,” as Wall Road expects affirmation from some chip makers within the coming earnings season that gross sales will endure from overbought stock.

“The ‘peak cycle’ vs ‘stronger for longer’ debate is not a debate with multiples collapsing amid double ordering worries, client weak point, inflation, macro, and new headwinds (Shanghai, Ukraine and so on.), and buyers are actually actively looking for estimate cuts,” Rasgon stated.

Learn: The tip of one-chip wonders — Why Nvidia, Intel and AMD’s valuations have skilled huge upheaval

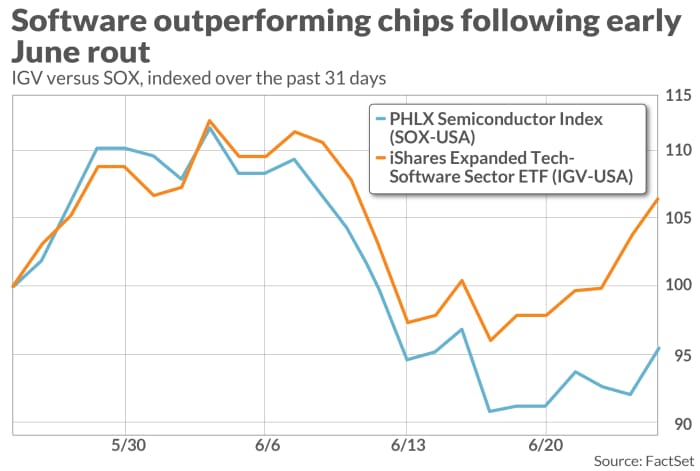

Klein tracked the disinvestment from chips into the software program sector, noting that software program shares have bounced again significantly higher than chip shares from the broad selloff within the first half of June. Klein stated he’s seeing a “main rotation” out of chip shares, following a rotation out of power and supplies shares.

Over the previous 31 days, the iShares Expanded Tech-Software program Sector ETF

IGV,

is up greater than 6%, whereas the PHLX Semiconductor Index

SOX,

is down greater than 4% over the identical interval. 12 months-to-date, the IGV is down 28% and the SOX index is down greater than 31%.

Compared, the Vitality Choose Sector SPDR ETF

XLE,

is down practically 15% over the previous 31 days, although it’s the one State Road SPDR sector ETF that’s in optimistic territory for the 12 months, with a 30% acquire. Equally, the Supplies Choose Sector SPDR ETF

XLB,

is down 9% over the previous 31 days, however not like power, the supplies ETF is down practically 17% for the 12 months.

“How a lot of that is actually true shopping for stays in query,” Klein famous. “Feels far more squeezy as rates of interest have pulled again and progress issue working vs the inflation winners.”

Mizuho’s money fairness desk, nevertheless, noticed a key pattern on Thursday of “actual measurement promoting” of power shares, and a few “actual shopping for in excessive progress software program.”

“Undecided if that is cash coming into software program fearing a sustained transfer greater in sector or simply extra dumping semis anticipating poor guides and affirmation that demand/orders are slowing,” Klein wrote, including that current conversations over the previous week point out that buyers have gotten much more unfavorable about chip shares.

Opinion: These 7 semiconductor shares could also be near a backside. This chart sample reveals when and the way a lot they could rebound.

On Tuesday, Morgan Stanley resumed protection of AMD with an chubby score, now that the funding agency is completed advising Xilinx following its acquisition by AMD, however that optimism didn’t lengthen as a lot to different chip makers. For its half, at AMD’s analyst day two weeks in the past, the chip maker caught to its outlook issued in Might, and stated it expects common annual progress of about 20% over the subsequent three to 4 years.

This previous earnings season Intel Corp.

INTC,

doubled down on its bullish 2022 outlook although the present quarter reveals indicators of weak point. And on Wednesday, Intel delayed its groundbreaking ceremony for its Ohio fab as enthusiasm in Congress to assist the chip business seems to have waned.

Learn: Intel wins newest race in chip makes use of for the cloud, says KeyBanc Capital Markets

Qualcomm Inc.’s

QCOM,

outlook was bullish, however analysts may see assist within the brief time period given energy in its handset enterprise. Nvidia lower its outlook due to China shutdowns and misplaced Russia income due to the battle in Ukraine, and Wall Road took that because the long-awaited “lower” for the inventory. Cisco additionally issued a poor outlook due to the China shutdowns and shares noticed their worst day in additional than a decade.

Chip-equipment suppliers had been much less optimistic due to persevering with provide chain issues holding them again. That was the case with Utilized Supplies Inc.’s

AMAT,

ASML Holding NV

ASML,

Lam Analysis Corp.

LRCX,

and KLA Corp.

KLAC,

[ad_2]

Source link