[ad_1]

Transferring into late summer time, the one certainty within the markets is uncertainty. The July jobs report was strong, however companies proceed to take care of a cussed labor scarcity. The Biden Administration appears like it should get what it desires from Congress, within the type of a $1 trillion infrastructure invoice and the $3.5 trillion finances bundle, however inflation is rising and the huge infusion of presidency spending will probably make that worse. It appears for each market argument, there’s a counter-argument.

The bull aspect within the present surroundings is ably set forth by Goldman Sachs chief US fairness strategist David Kostin, who says, “We anticipate earnings development would be the main driver of U.S. fairness returns in 2H 2021 and 2022, because it has been to date this yr.”

Kostin goes on to offer his forecast for the S&P as we spherical out the earnings season. Kostin expects general earnings per share amongst S&P-listed firms to achieve 45% year-over-year for the second quarter. In his view, the enhance in earnings will energy additional positive aspects within the index, which might climb over 4,700 – and perhaps attain as excessive as 4,950 – by yr’s finish. On a cautionary be aware, Kostin does warn in opposition to volatility within the coming months, because the Fed adjusts coverage.

Towards this backdrop, the analysts at Goldman Sachs have been in search of the equities primed to achieve in present situations. And only recently, they’ve tapped three shares new to the general public markets as more likely to bounce 60% or extra in coming months – a strong return that buyers ought to be aware. We ran the three by way of TipRanks database to see what different Wall Avenue’s analysts must say about them.

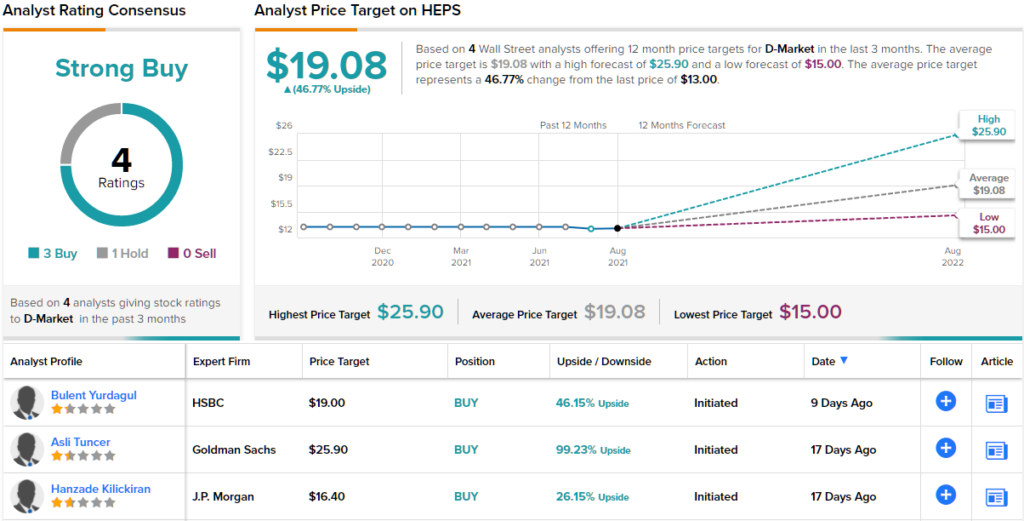

D-Market (HEPS)

We’ll begin with an organization from Turkey, D-Market, known as Hepsiburada in Turkish. D-Market is a number one e-commerce platform in Turkey, connecting prospects with retailers on an enormous scale. The corporate boasts over 50 million merchandise in its catalogs, and in 2020 linked 33 million member consumers with 45,000 lively retailers. The corporate’s Turkish model title interprets into English as ‘Every little thing is Right here.’

D-Market made a little bit of market historical past in July, when it turned the primary Turkish firm to achieve a public itemizing on the NASDAQ index. The IPO, which noticed the inventory begin buying and selling within the US on July 1, was formidable: the corporate wished to lift over $680 million in new capital and hit a valuation over $3 billion. Within the occasion, it beat these targets, elevating $738 million in gross proceeds and reaching a market cap of $3.9 billion. After a month and half of buying and selling, the corporate’s market cap now stands at $4.2 billion.

This firm has drawn consideration from Goldman Sachs analyst Asli Tuncer who sees the expansion profile as a key level right here.

“HepsiBurada is the second largest e-commerce platform in Turkey, an early-stage e-commerce market with penetration at present solely at c.10%. We see this accelerating to c.22% by 2025, a key driver of our forecast of a c.57% CAGR in HepsiBurada’s GMV over 2020-25 with the corporate’s lively person base and order frequency per person CAGRs at c.22% and c.27% respectively,” Tuncer wrote.

The analyst added, “We anticipate HepsiBurada to succeed in constructive EBITDA by 2023, pushed by market enlargement and an rising share of classes with larger take-rates, noting that HepsiBurada was worthwhile over 2018-19. Margin enlargement coupled with the corporate’s damaging working capital mannequin and decrease capex depth put up 2022 ought to drive a rise within the web money place, in our view, to c.TRY11.7 bn by 2025.”

To this finish, Tuncer charges HEPS a Purchase together with a $25.90 value goal. Buyers stand to take residence about 99% achieve, ought to the goal be met over the following 12 months. (To observe Tuncer’s observe document, click on right here)

General, there are 4 current analyst evaluations on file for HEPS, together with 3 to Purchase in opposition to a single Maintain. This offers the inventory a Robust Purchase consensus score. Shares are priced at $13, with a $19.08 common value goal that implies ~47% one-year upside. (See HEPS inventory evaluation on TipRanks)

Mix Labs (BLND)

The subsequent Goldman decide we’re is Mix Labs, a software program firm with a distinct segment in the actual property enterprise. The corporate provides a platform that permits a sooner, extra environment friendly residence shopping for course of for each patrons and lenders, and significantly facilitates mortgage lending. The corporate boasts that it could actually assist its prospects course of as much as $5 billion in new loans on daily basis, and has processed a complete mortgage quantity of $1.4 trillion since 2020.

These sort of numbers each drip money and promise development, and Mix used them as the idea for its IPO in July. The corporate priced the providing at $18 per share, with 20 million shares going available on the market and an underwriter possibility for a further 3 million shares. This was on the prime of the preliminary pricing estimates ($16 to $18), and the corporate raised $360 million within the providing. Nearly a full month after itemizing, Mix now has a market cap of simply over $4 billion.

At present, Mix has over 290 prospects, primarily monetary and lending establishments. Mix’s platform is obtainable to be used facilitating loans in a spread of industries, as the corporate has expanded from its actual property and mortgage roots. The corporate maintains a powerful connection to the actual property enterprise, and in June of this yr accomplished its acquisition of Title365, bought from the Mr. Cooper Group for $500 million.

Turning to Goldman Sachs, analyst Michael Ng initiated protection on BLND shares with a Purchase score and $30 value goal. This determine signifies his confidence in ~64% upside from present ranges. (To observe Ng’s observe document, click on right here)

“We forecast Mix to develop at 3-year consolidated income CAGR (2020-23) of 15% reflecting development in transaction quantity on the platform and enlargement of market place companies. This consists of 19%/-1%/30% income development in 2021/22/23, with the damaging development in 2022 primarily pushed by a decline in refinancing exercise again in the direction of pre-pandemic degree,” Ng opined.

The analyst continued, “Regardless of declining refinance transactions, (1) mortgage income ought to proceed to develop as Mix positive aspects market share. (2) Additional, Mix’s best-in-class know-how platform and expansive community of ecosystem companions ought to create a aggressive moat and drive additional income enlargement with current prospects. (3) Lastly, Mix ought to be capable of increase its TAM by constructing out its shopper banking and market choices.”

General, it’s clear that Wall Avenue agrees with Ng on the ahead prospects for Mix. The inventory’s 8 current analyst evaluations embody 7 Buys and 1 Maintain, for a Robust Purchase consensus indicative of a bullish outlook. The shares are priced at $18.18 and their $25 common value goal implies a 12-month upside of 37%. (See BLND inventory evaluation on TipRanks)

Full Truck Alliance (YMM)

For the final inventory, we’ll check out a Chinese language firm that has gone for a US itemizing. Full Truck Alliance is a digital freight platform, the biggest on the planet by gross transaction worth. It connects shippers in China with truckers, facilitating ships and street transport with a digitized normal and sensible logistics infrastructure. Some current numbers point out the scale of the enterprise: In 2020, Full Truck facilitated 71.7 million transport orders, and roughly 20% of China’s heavy- and medium-duty truckers used the platform that yr.

The corporate’s current 2Q21 report reveals that the 2020 numbers had been no outliers. Full Alliance reported US$173.3 million in complete revenues for the quarter, up 100.9% from the year-ago quarter. The gross transaction worth, or GTV, a key metric for the corporate, was up 57.8% year-over-year to US$11.5 billion. And at last, within the second quarter, truckers utilizing the platform fulfilled 36 million orders, up 87.9% from 2Q20.

The 2Q21 report was Full Alliance’s first as a public firm on the US markets. The corporate’s IPO opened on June 23 this yr, when 82.5 million American Depositary Shares (ADSs), every price 20 class A typical shares, had been made accessible to the general public at $19 per ADS. The underwriters had choices on a further 12.375 million ADSs.

Full Alliance met expectations within the sale. The IPO raised $1.6 billion within the largest US opening by a Chinese language firm to date this yr. As of mid-August, the corporate has a market cap of US$13.5 billion.

Goldman Sachs analyst Ronald Keung, in his be aware on YMM after the quarterly launch, noticed a number of factors indicating additional development for the corporate. First amongst these was the spectacular success charge.

“Continued enchancment in success charge to 30% in 2Q21, vs. 24% in 1Q21/17% in 2Q20, on the again of modern product options and repair upgrades, together with Faucet & Go and extra closed-loop transactions. Going ahead the corporate plans to proceed bettering its algorithm to raised match truckers and shippers, and additional elevate success charges,” the analyst famous.

Keung’s bullish outlook and Purchase score on the inventory include a $20.50 value goal, indicating his confidence in ~77% development for the yr forward. (To observe Keung’s observe document, click on right here)

Whereas there are solely 2 evaluations on document for YMM to date, they each agree that it is a inventory to Purchase, making the Average Purchase consensus score unanimous. The typical value goal is $20.50, matching Keung’s above, and the present buying and selling value is $11.56. (See YMM inventory evaluation on TipRanks)

To seek out good concepts for shares buying and selling at engaging valuations, go to TipRanks’ Greatest Shares to Purchase, a newly launched device that unites all of TipRanks’ fairness insights.

Disclaimer: The opinions expressed on this article are solely these of the featured analysts. The content material is meant for use for informational functions solely. It is extremely vital to do your individual evaluation earlier than making any funding.

[ad_2]

Source link