[ad_1]

Anybody feeling dizzy from the current market gyrations? Volatility is again on the menu in a giant means. The previous week noticed sturdy strikes in each instructions, with the bears in the end in management, culminating in Friday’s rout. After charging forward for a lot of the yr, the primary indexes have been on the backfoot not too long ago, with the market getting jittery over Omicron variant fears and the Fed’s hawkish flip. Friday’s seemingly disappointing jobs report additional fanned the flames of doubt.

Nonetheless, even amidst the uncertainty, there are at all times alternatives for traders keen to hunt them out.

The analysts at Raymond James have picked out 2 shares which they consider are primed to leap increased, on the order of 60% or higher. We’ve used the TipRanks platform to lookup the most recent information on these picks; seems the Road sees loads of upside too.

Cushman & Wakefield (CWK)

So let’s begin with an actual property firm. Cushman & Wakefield is a world participant in industrial actual property companies, and is without doubt one of the world’s largest such corporations, with complete income final yr of $7.8 billion. The corporate’s income is supported by a big portion of annual recurring charges, however it’s also uncovered to market cyclicity. In consequence, the inventory is extra more likely to acquire throughout the bull runs than extra steady investments similar to actual property funding trusts.

Yr-to-date, C & W shares have gained 27%, outpacing the S&P’s 21% acquire. The share positive aspects have come as the highest line has risen steadily by the yr. Revenues in Q1 had been reported at $1.9 billion; in Q3, revenues got here in at $2.3 billion, additionally representing a acquire of 20% yoy. Of the overall quarterly income, $1.7 billion was incurred from charges, up 28% from the prior yr. EPS for the third quarter was 34 cents, down from 50 cents in Q2 however up dramatically from the 4 cents reported in 3Q20.

Cushman & Wakefield is at all times looking out to broaden in inventive instructions, and in October of this yr the corporate introduced a partnership with WeWork, the versatile shared workspace firm. The partnership contains an funding by C & W of $150 million, and Cushman will be capable to leverage leasing and venture administration to create new income streams.

Additionally in October, Cushman entered a three way partnership with the industrial actual property finance firm Greystone. The enterprise will see Cushman put $500 million into Greystone’s Company, FHA, and Servicing companies, for a 40% stake.

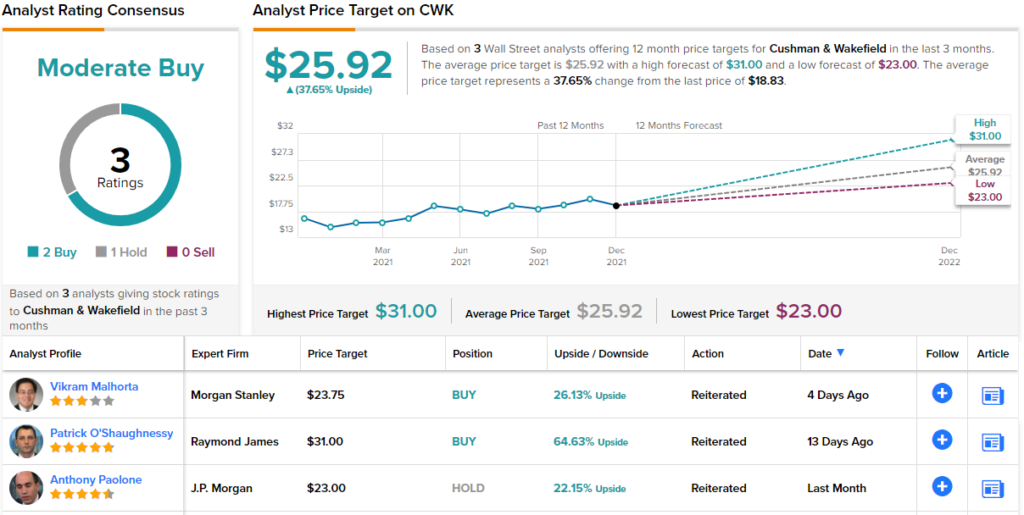

Masking CWK for Raymond James, 5-star analyst Patrick O’Shaughnessy writes, “We view Cushman’s present valuation to be extremely engaging each on an absolute and relative foundation, and we search for its pending funding in multifamily origination agency Greystone and partnership with WeWork as potential catalysts.”

O’Shaughnessy goes on so as to add that, “… regardless of an unclear medium-term outlook for workplace property demand, a rebounding world economic system is driving brokerage exercise increased and pointing in the direction of additional upside in 2022 and past.”

In keeping with these feedback, the analyst upgraded his view of the inventory from Outperform to Robust Purchase, and set a $31 value goal that means an upside of 64% for the yr forward. (To observe O’Shaughnessy’s monitor file, click on right here.)

This inventory holds a Average Purchase score within the Road’s consensus view, primarily based on 3 current opinions that embrace 2 Buys and 1 Maintain. The common value goal of $25.92 signifies a possible for 38% development from the present share value of $18.83. (See Cushman & Wakefield’s inventory evaluation at TipRanks.)

LianBio Sponsored ADR (LIAN)

The second inventory we’ll have a look at is a Chinese language biotech agency, LianBio. Not like many different clinical-stage biotech researchers, this firm is researching a diversified portfolio of recent drugs in a variety of fields. LianBio has scientific trials ongoing within the fields of respiratory, inflammatory, and heart problems, in addition to in oncology and ophthalmology. The applications are undertaken in partnerships with different world-class biopharma corporations.

The three main applications in LianBio’s pipeline are within the areas of oncology, heart problems, and ophthalmology. The main cardiovascular program is for mavacamten, first developed by Myokardia/Bristol Myers. Mavacamten accomplished a profitable Part 3 trial for the remedy of obstructive hypertrophic cardiomyopathy (HCM) within the US and a Chinese language Part 3 trial is ready to go forward throughout 1Q22.

Infigratinib leads the oncology program, indicated as a brand new remedy for gastric most cancers and different strong tumor malignancies. LianBio is working with BridgeBio Pharma on the scientific trials, and has three research ongoing. The drug has already been authorised in 2nd line cholangiocarcinoma within the U.S.

The corporate’s most superior program in ophthalmology is for TP-03, which was developed by Tarsus Prescribed drugs for the attention illness demodex blepharitis. Lian-Bio has made an settlement with Tarsus for growth and commercialization rights in China for the drug.

LianBio entered the US markets by an IPO on November 1 of this yr. The shares opened at $16 every, precisely in the midst of the anticipated vary, and the corporate raised $325 million on the sale of 20.31 million American depositary shares. Shares have made an inauspicious begin, sliding by 26% because the first day’s closing value.

Nonetheless, Raymond James analyst Dane Leone sees the three main analysis applications – and particularly the mavacamten program – as essential keys to LianBio’s ahead prospects. He outlines three factors for traders to contemplate: “1) LianBio has a tiered assortment of belongings with three considerably de-risked drug candidates together with mavacamten, TP-03, and infigratinib; 2) the corporate stands to quickly develop revenues starting 2025 with the anticipated approval of mavacamten, our projected main income driver; and three) the corporate has a diversified group of licensing companions, which grants it flexibility to pursue optimistic scientific outcomes whereas not relying too closely on one indication or drug class.”

Relating to mavacamten, Leone is bullish on the corporate’s capacity to commercialize, writing, “[LianBio] stands to begin gathering income throughout 2024 at $45M with a step as much as ~$320M throughout 2025.”

These feedback again up Leone’s Outperform (Purchase) score on the inventory, and his $27 value goal suggests an enormous upside of 168% from the present share value of $15.57. Leone’s is the primary assessment on file for this biotech inventory. (To observe Leone’s monitor file, click on right here.)

Different analysts see loads of upside too; going by the $24.4 common goal, shares are anticipated to rise by 142% over the approaching months. With 2 extra Buys vs. 1 Maintain, the inventory boasts a Robust Purchase consensus score. (See LianBio’s inventory evaluation at TipRanks.)

To seek out good concepts for shares buying and selling at engaging valuations, go to TipRanks’ Greatest Shares to Purchase, a newly launched device that unites all of TipRanks’ fairness insights.

Disclaimer: The opinions expressed on this article are solely these of the featured analysts. The content material is meant for use for informational functions solely. It is rather essential to do your individual evaluation earlier than making any funding.

[ad_2]

Source link