[ad_1]

The market’s key phrase heading into the previous couple of weeks of 2021 is ‘volatility.’ Because the starting of November, we’ve extra pronounced swings, each up and down, particularly on the NASDAQ index.

Watching the markets from Wall Road, the key banking corporations are discovering it onerous to return to settlement. There are bulls who say, ‘Purchase,’ however the bears are energetic, too. On that latter be aware, Morgan Stanley’s CIO of wealth administration, Lisa Shalett, writes: “We anticipate the S&P 500 to be range-bound and unstable, and bond returns to be damaging web of inflation… Traders ought to transfer towards inventory selecting and away from passive index funds.”

What this implies for retail traders is evident: take some proactive steps towards portfolio safety. A defensive transfer will present some cowl in an more and more unstable market surroundings, and the pure such transfer is to dividend shares. The regular earnings stream will assure a return, even when shares are slipping.

Utilizing TipRanks database, we’ve pinpointed two dividend shares which might be providing outperforming yields of seven% or higher. These are Sturdy Purchase shares, too, with latest optimistic rankings from the Road’s analysts and higher upside potential than is typical for high-yield dividend payers. Listed below are the main points.

Blackstone Mortgage Belief (BXMT)

We’ll begin with Blackstone Mortgage Belief, an actual property funding belief (REIT) focuses on mortgage mortgage packages relatively than direct actual property possession. Blackstone originates collateral-based senior loans, focusing on its investments within the North American, European, and Australian markets; the worldwide portfolio consists of 157 loans totaling $22 billion.

The corporate’s funding technique has been worthwhile; EPS in Q3 got here in at 63 cents, though flat from the yr in the past quarter. Up to now yr, EPS has held between 59 and 63 cents. Revenues have been rising this yr, from $185.7 million in Q1 to $198.5 million in Q3.

The optimistic earnings had been greater than sufficient to cowl Blackstone’s dividend, which has been held at 62 cents per frequent share for a number of years now. The corporate has an 8-year historical past of maintaining the cost dependable, and at $2.48 annualized, the dividend yields 8.2%. This compares favorably to the common dividend yield amongst S&P-listed shares, which is at the moment round 2%.

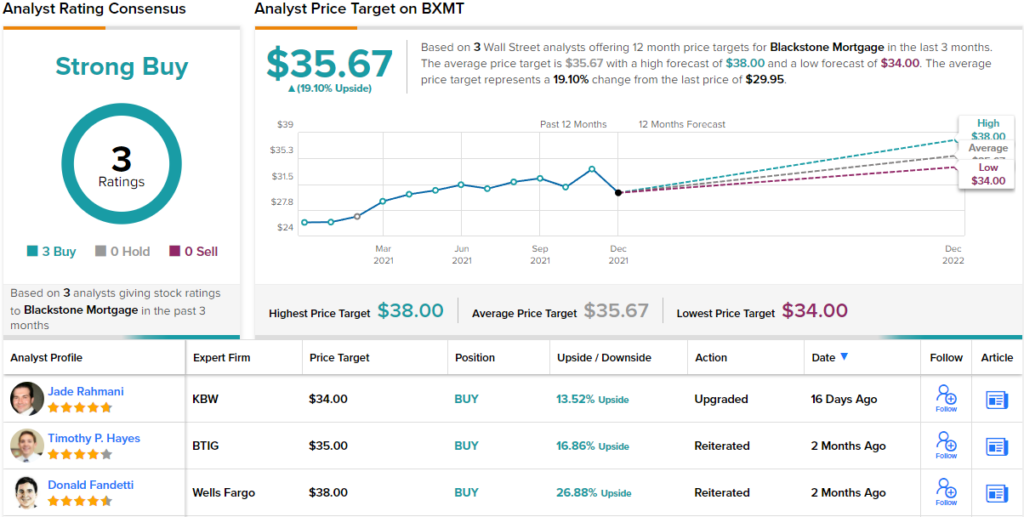

In protection for Wells Fargo, analyst Donald Fandetti lays out the bullish case for BXMT, writing, “It is optimistic to see quarterly earnings above the dividend as they proceed to maneuver previous the pandemic. Mortgage origination yields stay enticing regardless of extra competitors within the sector. We view BXMT as nicely positioned within the CRE lending markets given their relationship with personal fairness agency BX which is likely one of the largest actual property property homeowners on this planet. We imagine multiples will proceed to grind increased for the sector…”

Consistent with his optimistic method, Fandetti provides BXMT shares a Purchase score and his $15 worth goal suggests ~27% potential upside for the approaching yr. (To look at Fandetti’s monitor report, click on right here)

Whereas there are solely 3 latest opinions for this inventory, all of them agree: Blackstone Mortgage Belief is a inventory to Purchase, making for a Sturdy Purchase consensus view. The shares are buying and selling for $29.95 and their $35.67 common worth goal suggests a 19% upside within the subsequent 12 months. (See BXMT inventory forecast on TipRanks)

Starwood Property Belief (STWD)

The second inventory we’re is Starwood, one other actual property funding belief (REIT). These firms are well-known for his or her dependable and excessive dividend funds. The corporate’s important focus is industrial mortgages, but it surely additionally has investments in residential and infrastructure loans. Total, Starwood reaches $17 billion in complete investments.

Starwood’s earnings have been recovering for the reason that low level within the spring of final yr. Q3 EPS got here in at $51 cents — the very best in over two years. The corporate’s monetary outcomes had been greater than sufficient to maintain the dividend cost of 48 cents per frequent share, a cost that has been held regular for a number of years now. The dividend annualizes to $1.92 and yields a powerful 7.7%.

Among the many bulls is BTIG analyst Tim Hayes who’s upbeat on the corporate’s prospects.

“Thus far in 4Q21 (as of 12/3), STWD has deployed $3.2B throughout its funding methods, and we anticipate the corporate might be in retailer for a report quarter of funding given a sturdy ahead pipeline and powerful liquidity place. We imagine STWD is uniquely place to realize market share within the multifamily lending market given its potential to be extra versatile with underwriting than banks/insurance coverage firms and never simply depend on trailing information in underwriting. As such, we anticipate the multifamily market will provide an outlet for important capital deployment and enticing risk-adjusted returns,” Hayes opined.

“We view shares of STWD to be attractively valued, now buying and selling beneath 1.2x our year-end e-book worth estimate of ~$21.20/share and at a 7.7% dividend yield — a really enticing yield with the corporate being nicely positioned to face increased charges, inflation, and/or market volatility,” the analyst summed up.

These feedback assist Hayes’ Purchase score, and his $29 worth goal signifies potential for a 25% upside within the yr forward. (To look at Hayes’ monitor report, click on right here)

Total, it’s clear that Wall Road agrees with the bullish tackle Starwood. The inventory has 4 latest analyst opinions, they usually all agree that it’s a Purchase proposition, for a Sturdy Purchase consensus score. The common worth goal of $30.50 implies a one-year upside of 31.5% from the present buying and selling worth of $23.19. (See STWD inventory forecast on TipRanks)

To seek out good concepts for dividend shares buying and selling at enticing valuations, go to TipRanks’ Greatest Shares to Purchase, a newly launched device that unites all of TipRanks’ fairness insights.

Disclaimer: The opinions expressed on this article are solely these of the featured analysts. The content material is meant for use for informational functions solely. It is vitally necessary to do your individual evaluation earlier than making any funding.

[ad_2]

Source link