[ad_1]

We all the time appear to make new lists on the New Yr, and this yr isn’t any exception. Wall Avenue’s analysts are scouring by the markets, discovering the shares they like, and placing collectively their lists of ‘High Picks,’ the equities they see as the perfect of the pack heading into January.

We will get a taste for the standard of their recommendation by turning to Cowen, one of many Avenue’s main funding companies. Three of the agency’s prime analysts, all rated 5-stars from TipRanks, have chosen the shares they see as ‘prime picks,’ and their feedback make for attention-grabbing learn. Let’s take a more in-depth look.

Quanterix Company (QTRX)

We’ll begin with Quanterix Company, an organization within the life sciences area of interest, utilizing new strategies in ultra-sensitive digital immunoassay platforms to generate precision analysis and diagnostics. Quanterix bases its diagnostic platforms on a propriety know-how, Simoa, and affords a spread of devices an assay kits for improved diagnostic testing and lab work. The testing devices are designed to allow earlier illness detection, permitting enhanced remedy and extra profitable affected person outcomes.

In November, the corporate introduced that its Simoa know-how had proven vital advantages in medical trials for the remedy of Alzheimer’s illness. By making out there the use the plasma biomarkers in diagnostic testing, the tech permits researchers to focus their trials on sufferers with an earlier stage of the illness, for a extra environment friendly trial enrollment.

Factors like that assist to clarify Quanterix’s fourth yr in a row on the Deloitte Know-how Quick 500 listing. This can be a listing of the fastest-growing North America corporations within the fields of tech, fintech, power tech, life sciences, telecom, and media.

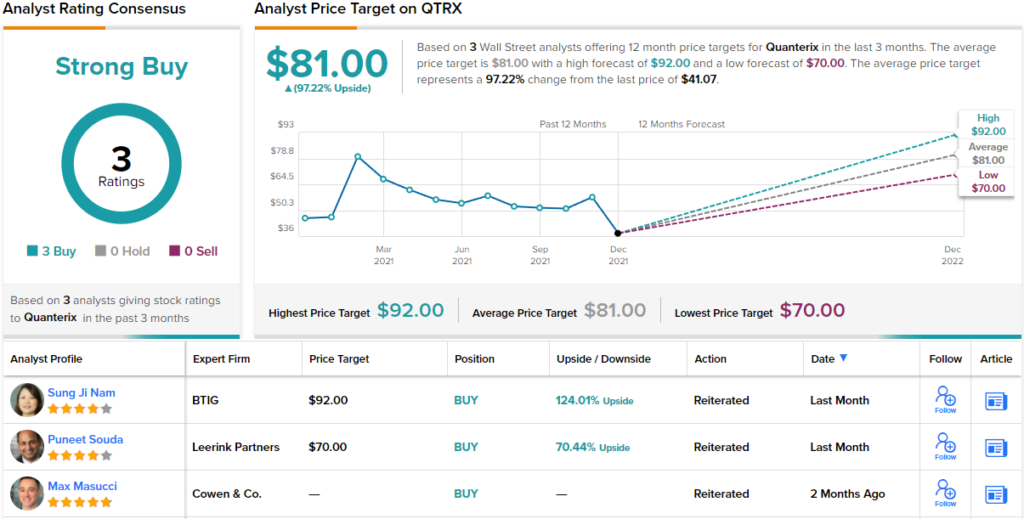

Whereas Quanterix is bringing in accolades, the shares are literally down this yr. The corporate’s inventory has fallen 55% from its February peak. And, along with the falling inventory, the corporate’s revenues are down, with the highest line in 3Q21 coming in at $27.7 million, 11% decrease than within the year-ago quarter.

Cowen analyst Max Masucci, nonetheless, nonetheless sees this inventory as a robust selection. He writes, “We imagine the precise position QTRX serves as a next-gen focused proteomics supplier is underappreciated and considerably misunderstood. Pushed by a catalyst-rich 2022 (at a company-specific and business stage), we anticipate appreciation for QTRX’s know-how (and its profit to researchers, biopharma, and down the highway, sufferers) to rise, which ought to assist to slender the hole between QTRX’s a number of and the peer common and drive beats versus conservative consensus estimates.”

These feedback again up Masucci’s Outperform (i.e., Purchase) score, and his $60 worth goal implies an upside for the approaching yr of 46%. (To observe Masucci’s observe file, click on right here)

General, the Wall Avenue view on Quanterix is bullish, primarily based on a unanimous 3 optimistic scores giving a Robust Purchase consensus view. The shares are priced at $41.07 and their $81 common worth goal suggests an upside of ~97% for the subsequent 12 months, even larger than the Cowen analyst permits. (See QTRX inventory evaluation at TipRanks)

BioMarin Pharmaceutical (BMRN)

Subsequent up is BioMarin, a California-based biopharma researcher concerned within the discovery, improvement, and commercialization/advertising and marketing of recent remedies for uncommon illness circumstances. The corporate’s particular focus is on genetic illnesses with debilitating or life-threatening signs – and few or no present remedies.

BioMarin has seven FDA-approved medicine available on the market, which introduced in a complete of $1.84 billion in income final yr. That complete was up 8% from 2019’s $1.7 billion. In 3Q21, the corporate had $408.7 million in revenues, whereas BioMarin’s largest vendor, Vimizin, the primary remedy for Morquio A syndrome, introduced in over $136 million of that income. In one other brilliant spot, BioMarin completed the quarter with $1.54 billion in liquid belongings, up 14% from the top of 2020.

On a detrimental observe, nonetheless, the Q3 income was down nearly 14% year-over-year. Administration famous that pandemic results led to ‘uneven ordering patterns’ throughout the yr, impacting revenues. Wanting forward, the corporate is guiding towards full-year revenues within the vary of $1.82 billion to $1.88 billion.

BioMarin, along with its accredited line-up of merchandise, additionally has a stable pipeline of medication in improvement. There are six analysis applications ongoing, with 3 in preclinical testing, two in Section 1 trials, and one, BMN 270, in a Section 3 trial. BMN 270, a drug candidate referred to as valoctocogene roxaparvovec or roctavian, is on observe for a BLA resubmission in 2Q22. The sooner stage research have a wide range of catalysts anticipated within the coming months. BioMarin has a historical past of commercializing rapidly and successfully as soon as a drug is accredited; its most not too long ago accredited product, Voxzogo, bought the go-ahead from the FDA in November and is already available on the market.

Cowen’s Phil Nadeau believes that BioMarin can flip its inventory round and entice new capital with sturdy commercialization exercise. He writes, “We anticipate {that a} sturdy Voxzogo launch and FDA approval of Roctavian will return investor curiosity to BMRN. The truth is, our mannequin tasks that Roctavian and Voxzogo’s launches will drive a 15% income CAGR by 2026, among the many highest in worthwhile biotech. We’re optimistic that these fundamentals will make BMRN a prime performer over the subsequent 12 months…”

These feedback again up Nadeau’s Outperform (i.e. Purchase) score, whereas his $135 worth goal suggests the inventory has a 61% upside by the top of 2022. (To observe Nadeau’s observe file, click on right here)

The curiosity that Nadeau foresees is already growing on Wall Avenue – there are 15 scores on file for this inventory, and their 12 to three Purchase-Maintain breakdown provides a Robust Purchase consensus. The inventory is promoting for $83.79 and the $112.36 common worth goal implies a one-year upside of 34%. (See BMRN inventory forecast on TipRanks)

Cloudflare (NET)

Let’s wrap up the listing within the networking sector. Cloudflare is a web-based community operator, providing content material supply companies, area identify server companies, and net infrastructure and web site safety companies. On-line companies are a scorching merchandise in in the present day’s digital world, and Cloudflare’s annual revenues present that. The corporate introduced in $287 million in complete income for 2019, and noticed that rise to $431 million final yr. Cloudflare has reported a sequential acquire in income each quarter for the previous two years.

Even so, the corporate’s inventory is down 36% from its mid-November peak. There’s been a way available in the market’s currently that the corporate could have run-up quicker than was justified, and was due for a correction. The shares had gained 189% from the beginning of the yr to their peak worth.

The 3Q21 report, nonetheless, reveals that the corporate continues to be a development proposition. Quarterly income, at $172.4 million, was up nearly 51% yoy. Extra importantly, EPS hit the break-even – a optimistic improvement after operating constant losses for a number of years.

5-star analyst Shaul Eyal units out the Cowen view right here, offering a distinctly bullish tackle Cloudflare’s outlook: “We imagine it took traders lower than two years to view NET as not solely a SMB safety/infrastructure/ supplier however relatively an built-in international cloud platform supplier able to tackle names akin to AWS which is rapidly climbing into the high-enterprise enviornment. With ~1,300 giant prospects and over 50% of income generated from giant prospects, NET’s mission of constructing a greater Web turns into crystal clear.”

To this finish, Eyal provides NET shares an Outperform (i.e. Purchase) score, whereas his $250 worth goal signifies his confidence in an upside of ~80% for the subsequent 12 months. (To observe Eyal’s observe file, click on right here)

All in all, NET holds a Reasonable Purchase score from the analyst consensus. That is primarily based on 16 opinions, together with 7 Buys, 8 Holds, and 1 Promote. The inventory’s $198.36 common worth goal suggests it has room for ~43% development from the $139.05 buying and selling worth this yr. (See NET inventory forecast on TipRanks)

See what prime Wall Avenue analysts say about your shares >>

Disclaimer: The opinions expressed on this article are solely these of the featured analysts. The content material is meant for use for informational functions solely. It is vitally vital to do your personal evaluation earlier than making any funding.

[ad_2]

Source link