[ad_1]

Will 2022 be the 12 months the world economic system recovers from the pandemic? That’s the large query on everybody’s lips because the festive break involves an finish.

One complicating issue is that many of the newest main forecasts had been revealed within the weeks earlier than the omicron variant swept the world. At the moment, the temper was that restoration was certainly across the nook, with the IMF projecting 4.9% development in 2022 and the OECD projecting 4.5%. These numbers are decrease than the circa 5% to six% world development anticipated to have been achieved in 2021, however that represents the inevitable rebound from reopening after the pandemic lows of 2020.

So what distinction will omicron make to the state of the economic system?

We already know that it had an impact within the run-up to Christmas, with for instance UK hospitality taking a success as folks stayed away from eating places. For the approaching months, the mixture of raised restrictions, cautious customers and other people taking day without work sick is more likely to take its toll.

But the truth that the brand new variant appears milder than initially feared is more likely to imply that restrictions are lifted extra shortly and that the financial impact is extra reasonable than it may need been.

Israel and Australia, for instance, are already loosening restrictions regardless of excessive case numbers. On the similar time, nonetheless, till the west tackles very low vaccination charges in some elements of the world, don’t be shocked if one other new variant brings additional harm to each public well being and the world economic system.

As issues stand, UK thinktank the Centre for Economics and Enterprise Analysis (CEBR) revealed a more moderen 2022 forecast simply earlier than Christmas. It predicted that world development would attain 4% this 12 months, and that the overall world economic system would hit a brand new all-time excessive of US$100 trillion (£74 trillion).

The inflation query

One different huge unknown is inflation. In 2021 we noticed a sudden and sharp surge in inflation ensuing from the restoration of world financial exercise and bottlenecks within the world provide chain. There was a lot debate about whether or not this inflation will show short-term, and central banks have been coming beneath strain to make sure it doesn’t spiral.

Up to now, the European Central Financial institution, Federal Reserve and Financial institution of Japan have all abstained from elevating rates of interest from their very low ranges. The Financial institution of England, however, adopted the IMF’s recommendation and raised charges from 0.1% to 0.25% in December. That is too little to curb inflation or do any good moreover enhance the price of borrowing for corporations and to boost mortgage funds for households. That mentioned, the markets are betting that extra UK charge rises will comply with, and that the Fed may also begin elevating charges within the spring.

But the extra vital query relating to inflation is what occurs to quantitative easing (QE).

That is the coverage of accelerating the cash provide that has seen the most important central banks shopping for some US$25 trillion in authorities bonds and different monetary property lately, together with about US$9 trillion on the again of Covid.

Each the Fed and ECB are nonetheless working QE and including property to their steadiness sheets each month. The Fed is at the moment tapering the speed of those purchases with a view to stopping them in March, having lately introduced that it could carry ahead the tip date from June. The ECB has additionally mentioned it can cut back QE, however is dedicated to persevering with in the interim.

After all, the true query is what these central banks do in follow. Ending QE and elevating rates of interest will undoubtedly hamper the restoration – the CEBR forecast, for instance, assumes that it’s going to see bond, inventory and property markets falling by 10% to 25% in 2022. It will likely be attention-grabbing to see whether or not the prospect of such upheaval forces the Fed and Financial institution of England to get extra dovish once more – significantly whenever you issue within the continued uncertainty round Covid.

Politics and world commerce

The commerce warfare between the US and China seems to be more likely to proceed in 2022.

The ‘Part 1‘ deal between the 2 nations, wherein China had agreed to extend its purchases of sure US items and providers by a mixed US$200 billion over 2020 and 2021 has missed its goal by about 40% (as on the finish of November).

The deal has now expired, and the large query for worldwide commerce in 2022 is whether or not there might be a brand new ‘Part 2’ deal. It’s arduous to really feel significantly optimistic right here: Donald Trump could have lengthy since left workplace, however US technique on China stays distinctly Trumpian, with no notable concessions having been supplied to the Chinese language beneath Joe Biden.

Elsewhere, western tensions with Russia over Ukraine and additional escalation of financial sanctions towards Putin could have financial penalties for the worldwide economic system – not least due to Europe’s dependency on Russian gasoline. The extra engagement that we see on each fronts within the coming months, the higher it is going to be for development.

No matter occurs politically, it’s clear that Asia might be essential for development prospects in 2022.

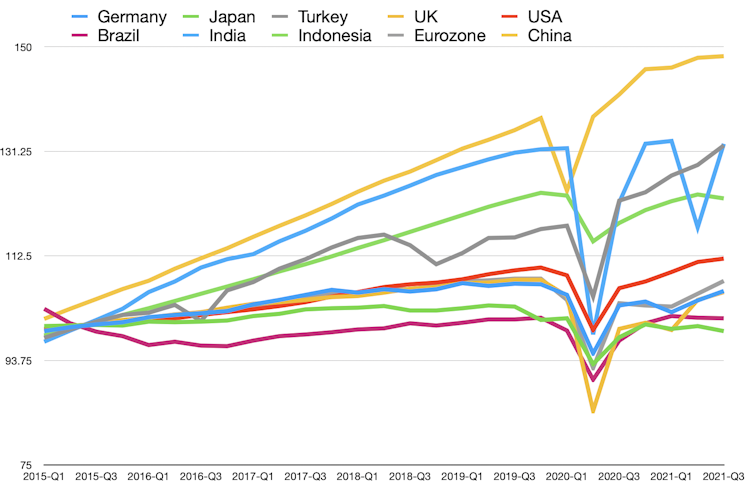

Main economies such because the UK, Japan and the eurozone had been all nonetheless smaller than earlier than the pandemic as lately because the third quarter of 2021, the newest information out there. The one main developed economic system that has already recovered its losses and regained its pre-Covid measurement is the USA.

Financial development by nation since 2015

Supply: OECD information

However, China has managed the pandemic properly – albeit with strict management measures – and its economic system has achieved robust development for the reason that second quarter of 2020. It has been battling a closely over-indebted property market, however seems to have dealt with these issues comparatively easily. Although the jury is out on the extent to which China’s debt issues might be a drag in 2022, some comparable to Morgan Stanley argue that robust exports, accommodative financial and financial insurance policies, aid for actual property sector and a barely extra relaxed strategy to carbon discount level to a good efficiency.

As for India, whose economic system has seen double dips through the pandemic, it’s exhibiting a powerful constructive pattern with 8.5% anticipated development within the 12 months forward. I subsequently suspect that rising Asia will shoulder world development in 2022, and the world’s financial centre of gravity will proceed to shift eastwards at an accelerated tempo.![]()

Muhammad Ali Nasir, Affiliate Professor in Economics and Finance, College of Huddersfield

This text is republished from The Dialog beneath a Inventive Commons licence. Learn the unique article.

[ad_2]

Source link

{kind=link}