[ad_1]

How do you make sense of the present market circumstances? We got here off a robust bull yr for shares with the worst January in a very long time – however the month ended, and February began with the perfect two-day motion since April 2000. And in a quirk, that buyers ought to notice, small-cap shares are displaying robust indicators of being closely oversold.

Small-caps took a tougher hit in January’s swoon than the market giants, and based on JPMorgan’s Chief International Markets Strategist Marko Kolanovic, buyers should purchase the dip.

“Small cap valuations are at 20Y lows, and investor sentiment is bearish. Many market metrics resembling latest efficiency of excessive vs. low beta shares and valuations of small caps are already absolutely pricing in a recession – one thing we don’t see materializing,” Kolanovic famous.

In opposition to this backdrop, we used TipRanks’ database to find a number of oversold small-caps which have obtained sufficient bullish assist from analysts to earn a “Sturdy Purchase” consensus ranking. The upside potential at play right here isn’t too shabby, both.

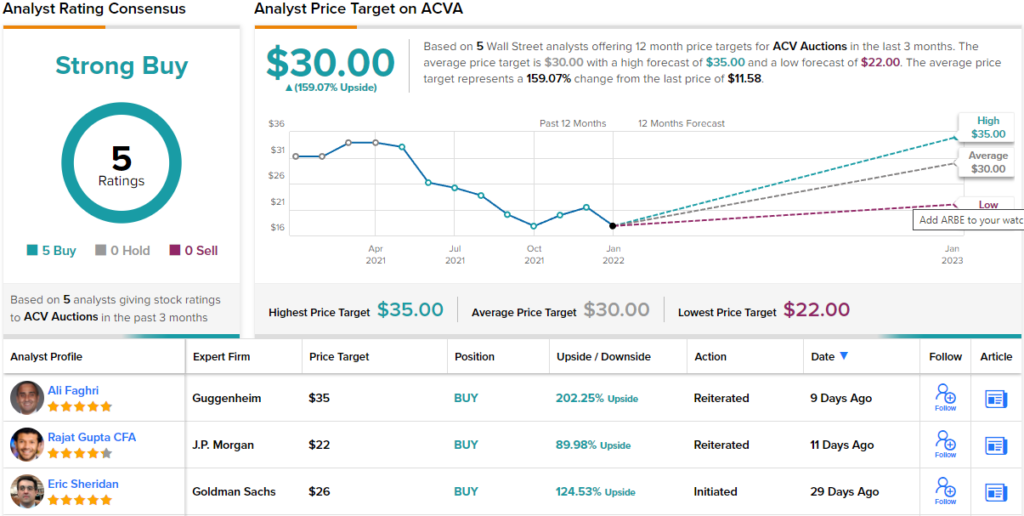

ACV Auctions (ACVA)

We’ll begin with ACV Auctions. This firm takes wholesale auto supplier public sale gross sales on-line, streamlining the method and bringing a successful mixture of transparency, velocity, and candor to the auto wholesale market. ACV is a holding firm, whose subsidiaries deal with the total vary of providers concerned in automotive wholesaling – from managing the auctions, to offering financing for patrons, to transporting autos, to offering unbiased third-party automobile inspections.

The corporate has been public for just below one yr, having held its IPO on March 24 of final yr. The preliminary providing noticed ACV put greater than 19 million shares in the marketplace, at a value of $25 every, and the corporate raised $414 million in new capital. For the reason that IPO, nonetheless, ACV inventory value has fallen by 63%.

Regardless of the autumn in share value, ACV has been reporting strong year-over-year income beneficial properties. Within the final quarter reported, 3Q21, the corporate confirmed $91.8 million on the high line, up 36% yoy. This included a 41% acquire in Market and Service income, which accounted for $78.3 million of the overall.

Trying ahead, ACV has pre-announced a few of its 4Q21 outcomes. The corporate expects income to beat the excessive finish of the beforehand printed $83 million to $86 million steerage; whereas down from Q3’s income, it will symbolize roughly 60% yoy development. The corporate additionally expects the EBITDA loss to average in This autumn. Official outcomes can be offered on February 16, and the corporate will maintain an analyst day on March 1.

Protecting ACV for Guggenheim, 5-star analyst Ali Faghri lays out a case for the inventory to surge, writing: “We consider ACV’s almost 100% publicity to supplier consignment positions it extra favorably from a quantity perspective, particularly into 2H22 and 2023 as new automobile SAAR begins to step by step rebound…. we consider it ought to proceed to ship robust quantity development because it takes share from bodily auctions, placing it in a greater place to navigate this tight provide backdrop.”

“We consider 2022 consensus estimates are achievable for ACVA and likewise see the March 1 analyst day as a optimistic catalyst the place the corporate ought to replace LT targets,” Faghri summed up.

In step with his bullish stance, Faghri charges ACVA a Purchase, and his $35 value goal implies room for a robust 202% upside for the yr forward (To observe Faghri’s monitor document, click on right here)

This inventory has a unanimous Sturdy Purchase ranking from the Wall Road consensus, with 5 optimistic critiques on file. The shares are promoting for $11.58 and their $30 common value goal suggests room for 159% appreciation within the subsequent 12 months. (See ACVA inventory forecast on TipRanks)

Arbe Robotics (ARBE)

Subsequent on our record is an organization within the autonomous automobile area of interest. Arbe Robotics was based in 2015 and has targeted its analysis and improvement work on the superior radar techniques self-driving automobiles have to ‘see’ their instant environments. Arbe makes use of a mixture of delicate radar expertise, strong processing tech, and superior algorithms to create an ultra-high decision system with the perfect efficiency on the roads. The corporate boasts that its radar techniques are as much as 100x extra delicate than current radars at present in use on self-driving automobiles. Arbe’ system, known as Phoenix, has a 300 meter vary, a 100 diploma azimuth, and 30 levels of elevation, and may differentiate between false alarms and true threats.

The corporate entered the general public markets in October of final yr, finishing a SPAC mixture at the moment with Industrial Tech Acquisitions. The ARBE inventory began buying and selling on the NASDAQ on October 8, and the corporate realized $118 million in gross proceeds from the transaction. The inventory rapidly surged to a peak above $14 in November, and has since fallen 48% from that degree.

Although the inventory has fallen, Arbe has had some strong wins to report in latest months. BAIC Group, a Chinese language auto producer, introduced in November that Arbe’s radar techniques are anticipated to be put in on BAIC Group’s new autos going ahead, and that very same month, Weifu, a Chinese language tier-1 auto elements provider launched a buyer road-pilot part of Arbe’s radar techniques and chipsets. Weifu expects to have the techniques in full manufacturing by the top of this yr.

And, in January, Arbe launched its radar primarily based free area mapping on the CES2022 exposition. The brand new mapping system is an addition to the imaging radar notion stack, and contains algorithms that permit the system to construct a map of the close to surroundings, with the automobile localized in it.

Analyst Josh Buchalter, from Cowen, sees Arbe constructing a strong basis within the automotive radar phase, writing of the corporate: “Arbe Robotics offers buyers the chance to personal an ADAS radar pure-play with sizable introduced auto wins… Whereas a lot of the funding neighborhood has targeted on lidar throughout the automobile autonomy area, Arbe’s options take part in a considerably much less aggressive radar market and may already be bought at <$200, a value auto OEMs can incorporate on high-volume autos.”

“Our checks within the sensing area reveal Arbe holds a big edge in radar decision, an vital enabling characteristic wanted to allow L2/L2+ autonomous options. For early development buyers, we consider the differentiated expertise, restricted competitors, and validating wins are indicators the story is simply starting,” the analyst added.

To this finish, Buchalter places an Outperform (i.e. Purchase) ranking on the inventory, together with a $15 value goal that means an upside of ~96% for the following 12 months. (To observe Buchalter’s monitor document, click on right here)

This inventory’s low value hasn’t deterred Wall Road’s analysts from staking out bullish positions. The inventory has a unanimous 3 critiques, for a Sturdy Purchase consensus ranking, and the typical value goal of $15.33 suggests a one-year upside of ~100% from the share value of $7.67. (See ARBE inventory forecast on TipRanks)

ALX Oncology Holdings (ALXO)

Final on our record is ALX, an immune-oncology biopharma engaged on CD47 blockers as a therapeutic goal in most cancers remedy. The corporate’s main drug candidate, evorpacept (also called ALX148) is the topic of no fewer than 6 scientific trials, as a remedy for a wide range of hematologic cancers and strong tumors. The drug candidate has proven anti-tumor exercise in a number of indications, and a suitable tolerability profile for sufferers.

The corporate has had a number of latest updates on its evorpacept packages, and launched the bulletins in January. The updates embody the anticipated initiation of a Part 2/3 scientific trial for the remedy of nice gastric/GEJ most cancers. This trial will consider evorpacept together with a number of different therapeutic brokers, together with Herceptin (trastuzumab), Cyramza (ramucirumab) and paclitaxel.

One other upcoming catalyst introduced in January considerations the Part 1b trial of an evorpacept-azacitidine combo within the remedy of MDS, myelodysplastic syndromes. The corporate can be releasing the dose optimization readout of this trial throughout this yr.

The ultimate January replace got here from the FDA, which granted evorpacept its Orphan Drug Designation within the remedy of gastric most cancers and gastroesophageal junction most cancers. Orphan Drug Designation comes with monetary advantages, together with tax credit and consumer payment exemptions for the corporate.

The scientific pipeline isn’t the one supply of optimistic updates for ALX. The corporate, in its January company replace, reported having $385.1 million in money available on the finish of 3Q21. At present spending charges, that is anticipated to maintain the corporate working trough the center of 2024.

Regardless of the optimistic announcement and upcoming catalysts, ALXO shares are down 83% within the final 12 months.

Nonetheless, Piper Sandler analyst Christopher Raymond is bullish, saying of ALX: “We proceed to love the continued progress throughout the pipeline for evorpacept, with plenty of catalysts on faucet for 2022 and extra readability round longer-term readouts famous in the present day. Total, given the place the inventory is at present buying and selling, we consider this title continues to be undervalued and stay patrons.”

Raymond makes use of his feedback to again an Chubby (i.e. Purchase) stance right here, and his $77 value goal signifies confidence in a sky-high 464% one-year upside potential. (To observe Raymond’s monitor document, click on right here)

Raymond isn’t the one bull right here, because the 6 latest critiques break down 5 to 1 in favor of Buys over Holds and provides a Sturdy Purchase consensus view. The inventory is promoting for $13.65 and its $70 common value goal implies an upside of 413% by the top of 2022. (See ALXO inventory forecast on TipRanks)

To seek out good concepts for shares buying and selling at engaging valuations, go to TipRanks’ Greatest Shares to Purchase, a newly launched software that unites all of TipRanks’ fairness insights.

Disclaimer: The opinions expressed on this article are solely these of the featured analysts. The content material is meant for use for informational functions solely. It is rather vital to do your personal evaluation earlier than making any funding.

[ad_2]

Source link