[ad_1]

After a interval of sustained losses, the inventory market has been staging a comeback, with valuations throughout the board shifting in a single path – increased. Between March 14 and March 23, the S&P 500 rose ~8%, whereas the NASDAQ was up ~12%.

Oppenheimer’s Chief Funding Strategist John Stoltzfus provides a proof for the highly effective rally: “In our view it wasn’t a lot that investor sentiment had turned broadly constructive final week however quite that sufficient traders began to see quite a few positives amongst financial knowledge factors and company administration commentaries and actions to offset a deluge of worries which have dogged the markets since early this yr.”

Actually, the key fairness benchmarks are actually above the degrees they had been when Russia first invaded Ukraine, suggesting to Stoltzfus that “projections of the affect on the US from the hostilities in Jap Europe have been overblown.”

Traders will likely be maintaining a tally of a variety of financial and macro knowledge introduced this week to see if that rally was only a one-off or if sentiment has really turned. Within the meantime, Stoltzfus continues to “favor equities within the present transitional setting.”

With this in thoughts, the inventory analysts at Oppenheimer have made it simpler to seek out equites which can be notably promising. They’ve pinpointed two names which they imagine are able to blast increased – within the order of at the very least 90%. Utilizing the TipRanks database, we will get thought what the remainder of the Road thinks lies in retailer for these shares. Let’s take a more in-depth look.

aTyr Pharma (LIFE)

We’re speaking about at the very least 90% features and the pure place to show to for such mercurial returns would be the biotech house. aTyr Pharma is an early-stage biotech which goals to show distinctive organic pathways into novel medicines for higher affected person outcomes.

The corporate is an skilled in tRNA synthetase and NRP2 biology; the main target of its analysis is on the extracellular performance and signaling mechanisms of tRNA synthetases. With greater than 300 protein compositions patented, aTyr has established a world mental property property directed to all 20 human tRNA synthetases and a few related signaling pathways.

aTyr has a number of candidates within the early levels of growth however the lead program is efzofitimod — the primary tRNA synthetase-derived and NRP2-targeting remedy.

The corporate is engaged on efzofitimod as a possible disease-modifying therapy for sufferers with severe inflammatory lung ailments with excessive unmet medical want. This contains interstitial lung illness (ILD), a class of uncommon immune-mediated lung ailments that may result in lung fibrosis. Pulmonary sarcoidosis – a typical type of ILD – was chosen as the primary medical indication.

In america, virtually 200,000 individuals have pulmonary sarcoidosis, which accounts for greater than 90% of all sarcoidosis instances. Efzofitimod has been designated orphan drug standing for this indication.

Following sturdy Part 1b/2a knowledge, encouraging suggestions from the sufferers and physicians and a constructive EoP2 assembly with the FDA, aTyr plans on initiating a pivotal trial in pulmonary sarcoidosis (PS) in 3Q22.

The drug’s promise and the pipeline’s potential have piqued Oppenheimer’s Hartaj Singh’s curiosity. He writes: “Compelling Part 1b/2a knowledge, clinicians’ constructive angle to the info, and a excessive unmet want give us conviction that the subsequent pivotal trial may transfer sooner than anticipated. We spotlight administration execution and imagine there may be extra upside to the story… As we layer in different ILDs in 2022, we see upside. And this isn’t but coupled with alternatives to increase into extra therapeutic areas like most cancers.”

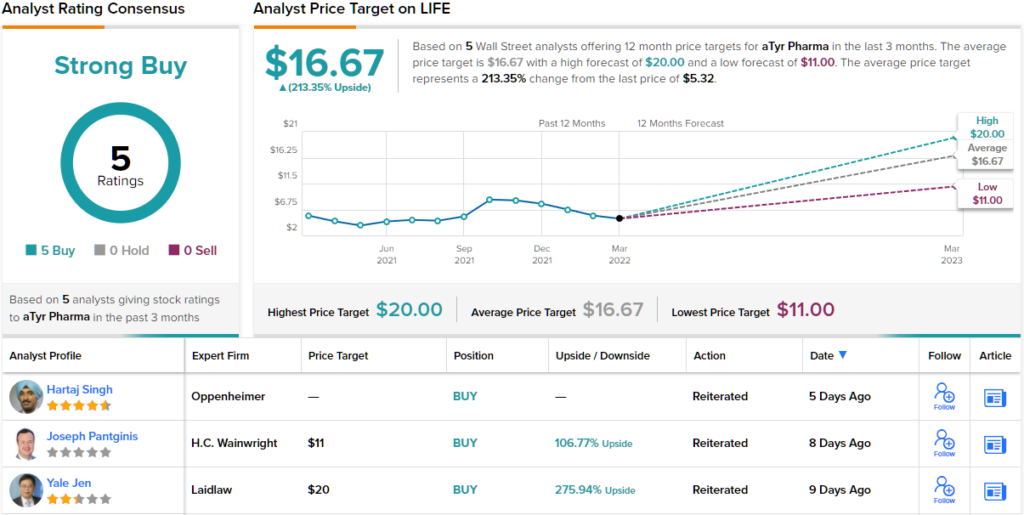

Certainly, Singh sees “upside.” Backing his Outperform (i.e. Purchase) ranking is a $21 value goal, which suggests room for 295% progress over the approaching yr. (To look at Singh’s observe document, click on right here)

4 different analysts have chimed in with evaluations just lately and they’re all constructive, making the consensus view on this inventory a Robust Purchase. Whereas not fairly as optimistic as Singh’s goal, the $16.67 value goal implies shares will nonetheless recognize by a hefty 213% within the months forward. (See LIFE inventory forecast on TipRanks)

Alpine Immune Sciences (ALPN)

We gained’t enterprise far a discipline for the subsequent inventory. Alpine Immune Sciences is a medical stage biotech engaged on the invention and growth of progressive, protein-based immunotherapies. These goal the immune synapse and are indicated for the therapy of most cancers and autoimmune problems. The corporate’s pipeline has applications in varied levels of growth, some in partnership with others and a few wholly owned.

Of be aware is the Synergy examine of Acazicolcept (ALPN-101), being developed in partnership with AbbVie with enrollment ongoing within the Part 2 trial of sufferers with SLE (systemic lupus erythematosus).

There’s additionally ALPN-303 – being developed for a number of autoimmune and/or inflammatory ailments. A Part 1 examine evaluating the protection, tolerability, pharmacokinetics, pharmacodynamics, and immunogenicity of the drug in wholesome volunteers started the enrollment course of in 4Q21.

The opposite program of be aware is for ALPN-202 (davoceticept) which is presently in two separate medical trials – NEON-1, as a monotherapy to deal with superior malignancies and NEON-2, together with pembrolizumab additionally indicated for adults with superior malignancies.

The latter has encountered some points just lately. The FDA has put a partial medical maintain on the examine following a affected person’s demise, attributed to cardiogenic shock, most likely associated to immune-mediated myocarditis.

Given myocarditis is a identified threat related to PD-1 inhibitors, Oppenheimer’s Mark Breidenbach estimates pembrolizumab is the “extra possible perpetrator on this case.” The analyst expects it would take between 3 to six months till enrollment for the examine resumes. Within the meantime, there are different catalysts to look ahead to.

“Whereas Alpine is working to resolve a medical maintain on the NEON-2 trial, we count on to see up to date dose-escalation knowledge from NEON-1 at AACR, the place we’d view clear security and proof of dose-dependent exercise in choose tumor varieties as a win,” the analyst mentioned. “By mid-year, we anticipate wholesome volunteer knowledge from ‘303, which may derisk Alpine’s plans to start trials in SLE and extra autoantibody-related ailments in 2H. We imagine Alpine is financed into early 2024, nicely past upcoming medical catalysts.”

To this finish, Breidenbach provides ALPN shares an Outperform (i.e. Purchase) ranking to go alongside a $17 value goal. The implication for traders? Upside of ~95%. (To look at Breidenbach’s observe document, click on right here)

Trying on the consensus breakdown, 3 Buys and no Holds or Sells have been issued within the final three months. Subsequently, ALPN will get a Robust Purchase consensus ranking. Based mostly on the $19 common value goal, shares may achieve ~118% within the coming months. (See ALPN inventory forecast on TipRanks)

To search out good concepts for shares buying and selling at enticing valuations, go to TipRanks’ Greatest Shares to Purchase, a newly launched instrument that unites all of TipRanks’ fairness insights.

Disclaimer: The opinions expressed on this article are solely these of the featured analysts. The content material is meant for use for informational functions solely. It is rather necessary to do your personal evaluation earlier than making any funding.

[ad_2]

Source link