[ad_1]

There are a a number of headwinds buffeting the markets proper now, pushing shares, bonds, and commodities in varied instructions. Between stubbornly excessive inflation, the struggle in Ukraine, the persistence of COVID, and even the creating instability in Chinese language actual property, the attainable shocks that may hit the market are sufficient to make any investor’s head spin. They’re additionally a powerful inducement to start out taking a defensive stance on an funding portfolio.

No less than, that’s the underside line from Morgan Stanley’s chief funding officer and US fairness strategist Mike Wilson. Wanting on the markets, and drawing conclusions, Wilson comes right down to a cautious take, saying, “We stay bearish on the S&P 500 index from a danger reward standpoint, notably after the latest rally. Our yr finish base case goal of 4400 is 4% under present ranges. On the inventory degree, we proceed to advocate traders search for secure money circulation producing corporations in defensive sectors.”

This can be a clear recipe for traders to observe, and can lead us fairly naturally to 2 latest inventory suggestions from Morgan Stanley’s analysts – for dependable dividend payers with enticing progress prospects. We ran each names by TipRanks’ database to see what different Wall Road’s analysts must say about them.

Agree Realty Company (ADC)

We’ll begin with a inventory in one of many market’s perennial dividend champion leagues, REIT. These corporations, actual property funding trusts, purchase, personal, function, and handle actual properties of all types – residential, multi-family, business, retail, industrial – in addition to investing in mortgages and mortgage-backed securities. Of curiosity right here to defensive-minded traders, REITs are required by governmental regulators to return a excessive share of earnings on to shareholders – and dividends are a typical mode of compliance. In consequence, REITs are recognized for providing dividends which are each high-yield and extremely dependable.

Metro Detroit-based Agree Realty focuses on proudly owning, creating, and leasing business properties for main retailers. The corporate boasts over 1,400 properties in its portfolio, totaling 29 million sq. toes and leased out to such main names as Autozone, Costco, Aldi, Finest Purchase, Walmart, and Sherwin-Williams.

In its most up-to-date reported quarter, 4Q21, Agree confirmed energy on a number of key metrics. The corporate’s high line income – derived primarily from property rents – got here in at $91.4 million, for the eighth consecutive sequential enhance. Yr-over-year, the highest line was up 28%. The corporate’s core funds from operations (FFO) was reported at 92 cents per share, whereas internet revenue got here out to 44 cents per share. These metrics grew by 10% and 5% y/y, respectively.

For a defensive investor, the important thing level to notice in ADC was the dividend. ADC pays out its dividend month-to-month, at 22.7 cents per widespread share. This annualizes to $2.72 per widespread share, and yields 4%. Whereas there are increased dividends on the market, what makes Agree stand out is its reliability – this firm has a saved up its funds, constantly, because it went public again in 1994.

Masking ADC for Morgan Stanley, analyst Ronald Kamdem opens his feedback on the inventory by stating the prime quality of Agree’s tenants, an vital differentiator for a REIT.

“Agree Realty Company has the very best high quality portfolio amongst triple internet REITs and a big runway for progress. ADC companions with industry-leading and rising retail tenants to offer them 1) progress capital by sale leasebacks and a pair of) improvement capabilities, the place ADC builds new shops for the retailer. The expansion alternative and the defensive traits of the enterprise stays underappreciated, we expect. Certainly, throughout the post-COVID interval, the a number of premium to friends has derated from +46% to +3%. Thus, we see a compelling entry level for this excessive money circulation, low capex, and defensive enterprise,” Kamdem opined.

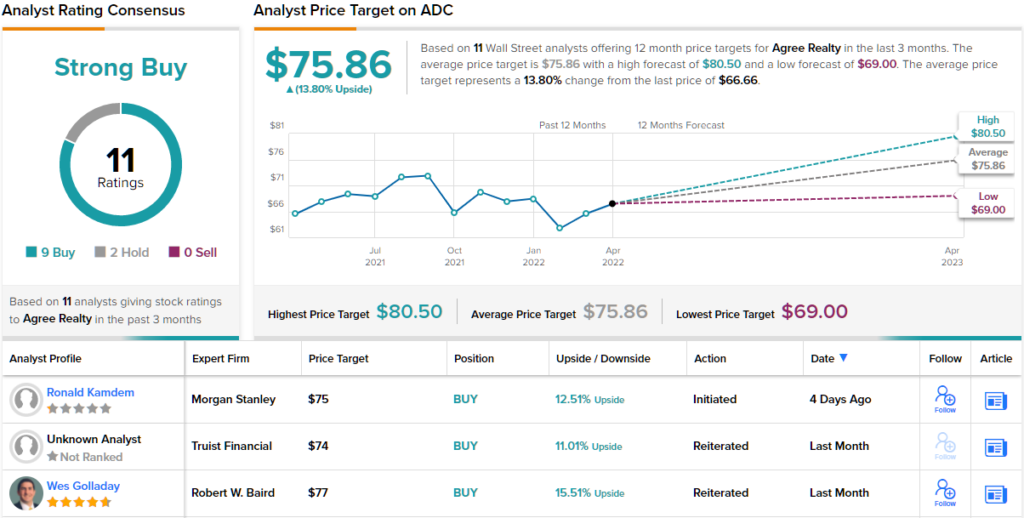

To this finish, Kamdem initiated protection on ADC shares with an Chubby (i.e. Purchase) score and $75 worth goal. The determine implies 12.5% upside from present ranges. (To look at Kamdem’s monitor document, click on right here)

Morgan Stanley is hardly the one agency to charge this REIT extremely; the inventory has 11 latest opinions they usually embody 9 Buys that overbalance 2 Holds. The shares are priced at $66.66, with a mean goal of $75.86 indicating ~14% one-year upside potential. (See ADC inventory forecast on TipRanks)

AT&T, Inc. (T)

The second dividend inventory we’ll have a look at wants no introduction. AT&T is blessed with one of many world’s most recognizable company manufacturers, and an extended historical past within the important telecom sector. In its fashionable incarnation, AT&T supplies landline phone companies, broadband web by fiber-optic and wi-fi networks, and is closely concerned in rolling out 5G within the US. AT&T boasts a market cap of $173 billion, and roughly $170 billion in annual revenues.

In latest months, AT&T made an attention-grabbing divestment transfer. The corporate acquired TimeWarner in 2018, however earlier this yr introduced that it’s spinning off its curiosity within the acquisition (now known as WarnerMedia) to shareholders, as a part of a merger between WarnerMedia and Discovery Inc. This merger will create a brand new leisure firm, Warner Bros. Discovery, and AT&T shareholders will every obtain 0.24 shares of the brand new firm for each share of AT&T inventory owned.

Along with the inventory spinoff, AT&T has additionally declared a inventory dividend, to be payable in Might. The dividend was set at 27.75 cents per widespread share, or $1.11 annualized, and yields 4.63%. The dividend is supported by AT&T’s substantial free money circulation, which was reported in 4Q21 as $8.7 billion, and for the complete yr of 2021 as $26.8 billion. Simply as vital is the reliability of the dividend; AT&T has demonstrated a long-term dedication to maintaining the funds, and has not missed a quarterly dividend for the reason that funds have been initiated 38 years in the past in 1984.

Analyst Simon Flannery, masking this inventory for Morgan Stanley, lately attended an AT&T investor day, and wrote of the occasion, “We have been inspired with the improved visibility into free money circulation era and EBITDA progress over the following couple of years. AT&T is likely one of the greatest values in our protection universe with a professional forma dividend yield of over [4%], a double digit free money circulation yield, and a professional forma P/E a number of of simply 7x on newly issued steerage… We imagine the inventory may see incremental investor curiosity after the spin is full.”

Based mostly on the above, Flannery charges AT&T shares an Chubby (i.e. Purchase), with a worth goal of $28 to recommend an upside of ~16% within the subsequent 12 months. (To look at Flannery’s monitor document, click on right here)

All in all, the analyst consensus score here’s a Reasonable Purchase, primarily based on 14 opinions which embody 8 Buys, 5 Holds, and 1 Promote. The common worth goal of $29.69 implies an upside of ~23% from the $24.18 present buying and selling worth. (See AT&T inventory forecast on TipRanks)

To search out good concepts for dividend shares buying and selling at enticing valuations, go to TipRanks’ Finest Shares to Purchase, a newly launched software that unites all of TipRanks’ fairness insights.

Disclaimer: The opinions expressed on this article are solely these of the featured analysts. The content material is meant for use for informational functions solely. It is vitally vital to do your personal evaluation earlier than making any funding.

[ad_2]

Source link