[ad_1]

(Bloomberg) — The quickest inflation in many years and the ensuing rush by central banks to lift rates of interest are stoking recession fears in monetary markets — worries which can be being compounded by the impression of aggressive coronavirus lockdowns in China and the conflict in Ukraine.

Most Learn from Bloomberg

Within the final week alone, the the U.S. and U.Ok. logged inflation accelerating essentially the most because the early Eighties and the central banks of Canada and New Zealand offered a mannequin for the U.S. Federal Reserve and others by mountaineering charges 50 foundation factors for the primary time in 22 years.

Financial institution of America Corp. reported fund managers had been essentially the most bearish they’d ever been in regards to the outlook for progress and JPMorgan Chase & Co. boosted its reserves to insulate itself towards an financial deterioration.

Meantime, Sri Lanka and Pakistan fell deeper into crises because the United Nations warned of a “good storm” for growing nations as commodity costs surge, the World Commerce Group minimize its outlook for commerce and searches for “recession” on Google and the Bloomberg Terminal spiked.

In opposition to such a backdrop, coverage makers head to Washington this week for conferences of the Worldwide Financial Fund and World Financial institution. The Fund is already saying the conflict means it can downgrade its forecasts for 143 economies this 12 months — accounting for 86% of worldwide gross home product.

“We face a disaster on high of a disaster,” mentioned IMF Managing Director Kristalina Georgieva.

What Bloomberg Economics Says…

“For the worldwide economic system, the mixed impression of conflict and coronavirus can be a 12 months of decrease progress, greater inflation and elevated uncertainty. To get to recession, we’d must see additional shocks. Russia slicing off Europe’s fuel provide or China’s lockdown increasing from Shanghai to different main cities are doable catalysts.”

— Tom Orlik, chief economist

However there are additionally causes to assume resilience, albeit with a contact of stagflation slightly than world recession, could be the order of the day, not less than for wealthy nations.

Because of pandemic-era stimulus, households in developed markets nonetheless have 11% to 14% of earnings in financial savings, in keeping with a JPMorgan Chase evaluation despatched to shoppers final week.

Leverage is at multi-decade lows and earnings is advancing at an annual charge of about 7% amid tightening labor markets, catalysts for a possible rebound within the second half of the 12 months. Within the U.S., reviews final week on retail gross sales and client sentiment supplied hope all customers aren’t pulling again regardless of value shocks.

“I see extra causes for the worldwide economic system to gradual than for it to re-accelerate,” mentioned Stephen Jen, who runs Eurizon SLJ Capital, a hedge fund and advisory agency in London. “Nonetheless, whether or not it can fall right into a recession is a complete totally different story, just because the abatement of covid around the globe ought to unleash big pent-up demand, serving to to offset a part of the headwinds.”

Nonetheless, that robustness goes to be examined.

The quickest inflation in many years around the globe is already beginning to flip off many customers, particularly these witnessing greater meals and gas payments. About 84% of People plan to chop again on spending due to greater costs, in keeping with a Harris Ballot for Bloomberg Information.

Central bankers are additionally pushing up rates of interest with the Fed now extra doubtless than to not enhance its benchmark by a half-point subsequent month for the primary time since Could 2000 and begin decreasing its portfolio of bonds. Chairman Jerome Powell is anticipated to deal with the outlook in an look on Thursday.

One hazard is that coverage makers flip from reacting too late to rising inflation to tightening an excessive amount of as their economies weaken or if inflation seems to be pushed by provide chain woes that financial coverage can’t handle. The fund managers surveyed by BofA noticed an 83% danger of a coverage error.

“The explanation we’re a lot slower progress is that central banks want to reply by tightening coverage from its presently very straightforward state such that monetary circumstances will tighten and that can restrain demand,” mentioned Karen Dynan, Senior Fellow on the Peterson Institute for Worldwide Economics.

In a precursor of the IMF’s new financial outlook to be launched on Tuesday, Dynan estimated world progress will gradual to three.3% this 12 months and subsequent, in contrast with 5.8% in 2021.

The large superior economies will develop solely reasonably this 12 months and weaken additional in 2023, she mentioned. Giant rising markets face a “divergent” outlook with India bettering and China grappling with lockdowns and a property downturn.

The tempo of developments this 12 months has caught policymakers off guard.

The White Home’s high financial adviser Brian Deese mentioned final week that the U.S. faces numerous uncertainty. China’s Premier Li Keqiang mentioned there’s an pressing want for presidency stimulus.

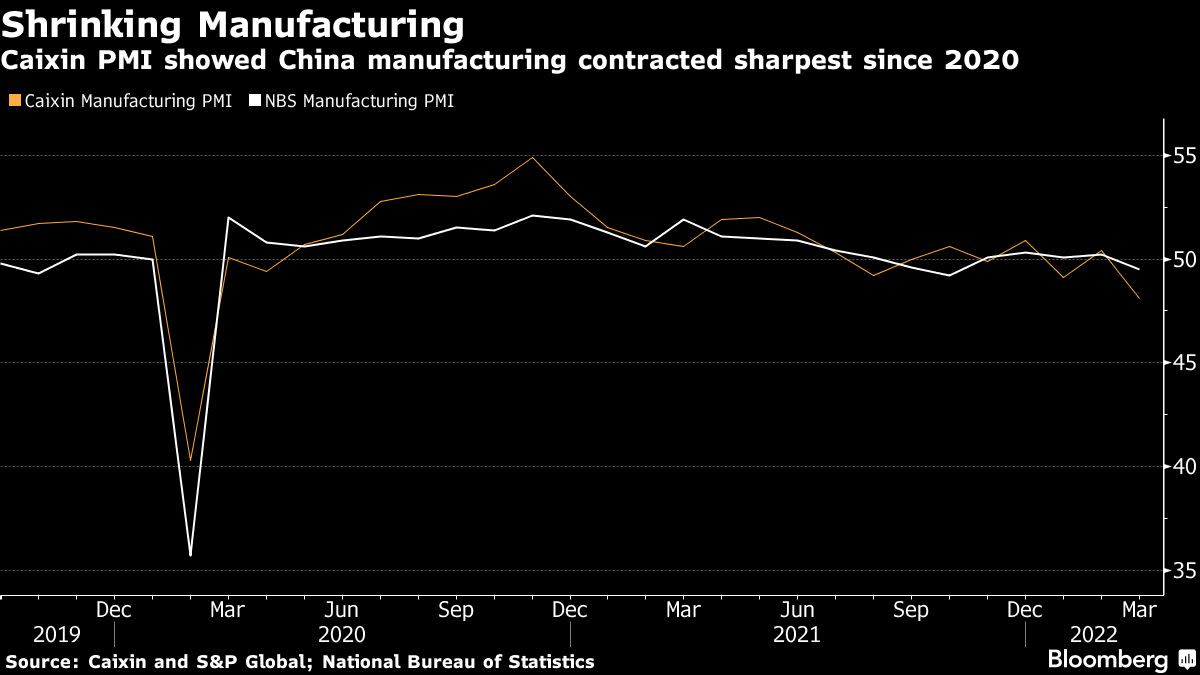

Russia’s invasion of Ukraine has overshadowed a deepening slowdown in China as the federal government continues with its “dynamic zero” method to controlling Covid-19, a coverage that has stalled manufacturing in manufacturing and monetary hubs Shenzhen and Shanghai and saved thousands and thousands of individuals at house.

That method, nevertheless, is more likely to push progress down to five% this 12 months, beneath the official goal of round 5.5%.

International provide strains that had been nonetheless recovering from the pandemic may undergo an extra setback if China doesn’t management the virus quickly.

Big Manufacturing Co. is among the many producers feeling disruption. It’s ready so long as two years for bicycle elements, Chairperson Bonnie Tu informed Bloomberg Tv.

“It’s a hell of job,” she mentioned.

Most Learn from Bloomberg Businessweek

©2022 Bloomberg L.P.

[ad_2]

Source link