[ad_1]

The inventory market continues to development decrease.

Earlier than rallying on Friday, the S&P 500 had a closing low of three,930.08 on Thursday, down 18.1% from its all-time closing excessive of 4,796.56 on January 3.

If you happen to contemplate the intraday market motion, the S&P traded as little as 3,858.87 on Thursday, down 19.9% from its intraday excessive of 4,818.62 on January 4.

Technically talking, shares don’t enter a “bear market” till costs are down a minimum of 20% from their highs. And for many market watchers, this calculation is predicated on closing costs. Frankly, that is all foolish semantics about spherical numbers and rounding errors.

Any method you take a look at it, the inventory market is down rather a lot.

Studying from historical past

We might debate all the ways in which the current day is and isn’t like historical past’s bull and bear markets, however that’s unlikely to finish with a definitive conclusion.1 Nonetheless, let’s do a fast overview of historic market efficiency.

Technically, we’re in 12 months three of a bull market that started on March 23, 2020.

Ryan Detrick, chief market strategist at LPL Monetary, reviewed the history and found that three of the 11 bull markets since World Conflict II resulted in 12 months three. So from the angle of length, it wouldn’t be too uncommon for shares to be in a full-blown bear market a while earlier than March 2023.

On the matter of length, historical past’s inventory market corrections (i.e., when the inventory market falls by greater than 10% however lower than 20%) have had a mean size of 133 days from market prime to market backside, in keeping with data compiled by Detrick.

The present correction has run for 131 days as of Friday, which makes it fairly near common assuming the market inflects upward quickly.

And since we’re very near being in a technical bear market, now is an efficient time to speak about historical past’s bear markets. Ben Carlson, director of institutional asset administration at Ritholtz Wealth Administration, reviewed the historic information.

Since 1950, the common bear market lasted 338 days (with a spread of 33 to 929 days) and noticed the S&P 500 fall a mean 30.2% (with a most decline of 56.8%).

It’s value noting that many — however not all — bear markets got here with financial recessions. And as you would possibly count on, the bear markets amid recessions tended to be worse.

Carlson noticed that since 1929, recessionary bear markets lasted a mean 390 days peak to trough, with shares falling a mean 39.4% throughout that interval. In the meantime, non-recessionary bear markets lasted a mean 202 days with shares falling a mean 26.1%.

That is what traders signed up for

When speaking to novices about investing within the inventory market, I attempt to make it some extent to say you can get smoked within the short-term. In reality, TKer Inventory Market Fact No. 2 is actually: “You will get smoked within the short-term.”2

Big inventory market sell-offs are regular. The S&P has traditionally seen a mean annual max drawdown (i.e. the largest intra-year sell-off) of 14%. Some years see milder sell-offs. Different years see worse ones.

This all speaks to 2 conflicting realities traders should deal with: In the long term, issues virtually at all times work out for the higher, however within the quick run, something and the whole lot can go mistaken. That is what investing within the inventory market is all about.

A observe in regards to the present second…

The financial information continues to be very robust, and there proceed to be huge tailwinds that counsel development will persist.

Equally, expectations for earnings development have been bettering. Taken with falling costs, valuations are more and more enticing.

As of Friday, the ahead P/E ratio on the S&P 500 was 16.6, in keeping with FactSet. That is beneath its 10-year common of 16.9.

This mix of resilient financial development, bettering earnings expectations, and enticing valuations has a minimum of some Wall Avenue professionals advising shoppers to tackle threat.

And historical past says that sell-offs just like the one we’re experiencing now, are sometimes adopted by sharp recoveries.

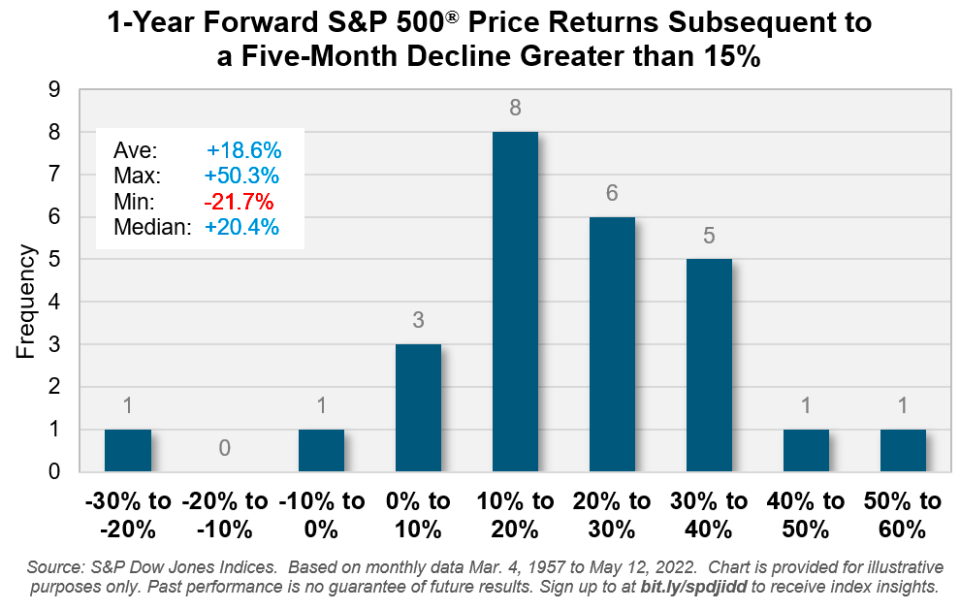

In accordance information from Benedek Vörös, director of index funding technique at S&P Dow Jones Indices, “a decline of 15% or extra [over a five-month period] for the S&P 500 has been adopted by constructive returns within the ensuing 12 months in all however two events over the previous 65 years, with a mean achieve simply shy of 20%.“

After all, there’s no assure that metrics proceed to maneuver favorably, particularly because the Federal Reserve actively strikes to chill demand within the financial system. And it’s actually attainable that shares proceed to fall, no matter what the information justifies.

However on stability, general situations proceed to look favorable for traders who’re in a position to put within the time.

—

Associated studying from TKer:

Rearview 🪞

📉 Shares hold falling: The S&P 500 declined 2.4% final week. The index is now down 16.1% from its January 3 closing excessive of 4796.56. For extra on market volatility, learn this and this.

Earnings development, nevertheless, stays agency, which has prompted valuations to become much more attractive. For extra on valuations, learn this and this.

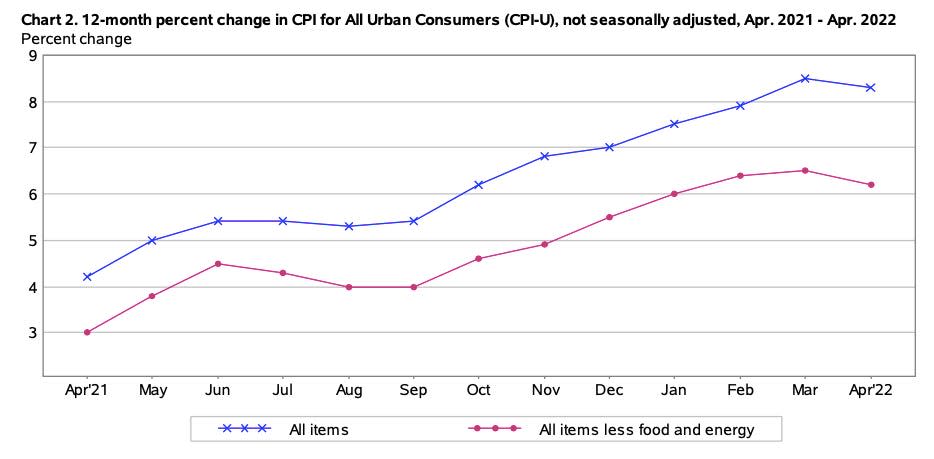

🎈 Inflation is excessive, however off its excessive: The patron worth index (CPI) climbed 0.3% in April from March. CPI is 8.3% above 12 months in the past ranges. Core CPI, which excludes meals and power, rose 0.6% month-over month, reflecting a 6.2% year-over-year achieve.

The decline within the annual figures helps the concept inflation could have peaked in March. Although, no one is able to have a good time but. “Regardless of the April information suggesting a peak might need been reached for y/y CPI, the renewed rise in gasoline costs in the direction of a report $4.50 nationally and improve in diesel costs indicators that there’s nonetheless upward threat to the inflation outlook,” Kathy Bostjancic, chief U.S. monetary economist at Oxford Economics, wrote on Tuesday. “Additional, the Covid-related China lockdowns and the continued Russia-Ukraine struggle locations additional stress on already strained provide chains.“

🤔 Some ideas on the CPI particulars: One of many classes that jumped out of the CPI report was airline fares, which spiked 18.6% month-over-month in April. That is no shock for anybody who’s traveled lately. There are lots of people going out and doing stuff. It’s a mirrored image of a booming financial system, not a stagnating one.

“Particulars confirmed stagflation is unlikely,” Paul Donovan, chief economist of UBS International Wealth Administration, mentioned on Wednesday. “Stagflation happens when an merchandise’s inflation will increase similtaneously demand falls… [The CPI] information confirmed that the place demand fell, inflation slowed or turned to deflation. If demand is rising, costs are rising. US airfares roared forward, reflecting an ongoing want to journey.”

“The U.S. financial system stays in an inflationary growth,” Neil Dutta, head of U.S. economics at Renaissance Macro, mentioned in an e-mail on Tuesday. “That’s the one technique to describe above consensus employment development and inflation over the month of April.”

If you would like a high-level take a look at how costs moved for some classes, take a look at the desk in my tweet. If you would like an in depth take a look at all the classes, you’ll be able to obtain the complete BLS reporter.

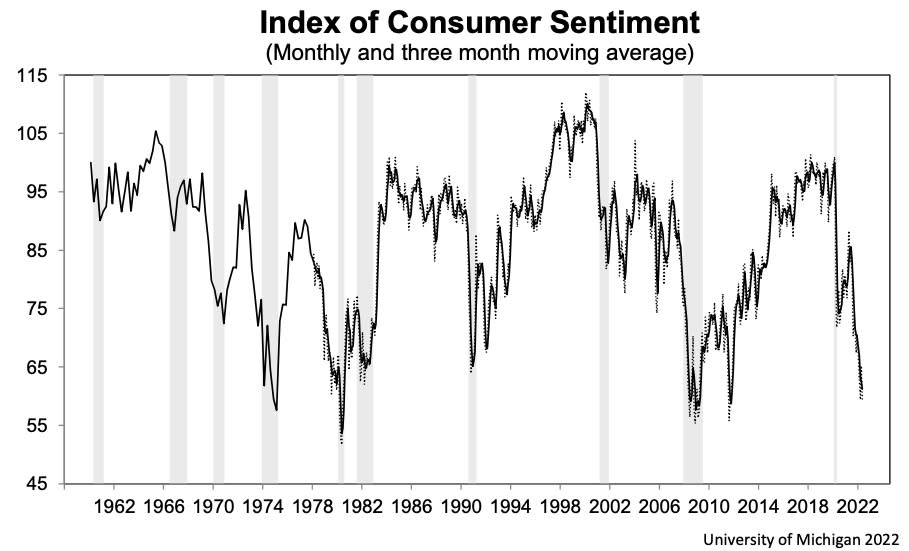

😤 Shopper sentiment tumbles: The College of Michigan’s index of client sentiment fell 9.4% to 59.1 in Could, its lowest stage since August 2011. From the survey: “Shoppers’ evaluation of their present monetary state of affairs relative to a 12 months in the past is at its lowest studying since 2013, with 36% of shoppers attributing their detrimental evaluation to inflation. Shopping for situations for durables reached its lowest studying for the reason that query started showing on the month-to-month surveys in 1978, once more primarily because of excessive costs. The median anticipated year-ahead inflation price was 5.4%, little modified over the past three months, and up from 4.6% in Could 2021.“

Needless to say deteriorating sentiment hasn’t include a decline in spending in latest months. For extra on sentiment, learn this.

Up the highway 🛣

It’s a giant week for client spending information, particularly following that gloomy client sentiment report.

On Tuesday, we’ll get the April retail gross sales report. Economists estimate gross sales climbed by 0.9% throughout the month. Excluding autos and gasoline, gross sales are estimated to have elevated by 0.7%.

The week additionally comes with earnings bulletins from Walmart, House Depot, Goal, Lowe’s, TJX Firms, Colgate-Palmolive, and Kohl’s.

Learn the newest monetary and enterprise information from Yahoo Finance

Comply with Yahoo Finance on Twitter, Fb, Instagram, Flipboard, LinkedIn, and YouTube

[ad_2]

Source link