[ad_1]

A lot has been fabricated from the headwinds the ecommerce section has come up towards in current instances. Continued provide chain and inflationary pressures amidst slowing client discretionary spending and the influence of the economic system’s reopening have all impeded the sector’s development.

And as was evident in a disappointing Q1 report, Amazon (AMZN) has felt the pinch too.

J.P. Morgan’s Doug Anmuth thinks the macro headwinds will nonetheless have a big half to play in Q2 – significantly within the first half – but as comps ease within the latter half of the yr, and Amazon makes additional headway in “key under-penetrated classes” comparable to grocery, CPG, attire & equipment, & furnishings/home equipment/tools, income development must also choose up steam in 2H22.

There may be additionally one other factor to contemplate when evaluating Amazon’s near-term prospects. The corporate has invested closely over the previous couple of years; the workforce has virtually doubled to 1.6 million, whereas the achievement community is now twice as giant. However the firm now seems to have an excessive amount of capability – each within the workforce and infrastructure sensible.

That mentioned, Amazon has already claimed this yr’s achievement capex could be decrease than final yr, whereas transport capex must also are available “flat to barely down.” The outcome needs to be an general discount of ~55% of the whole capex spend in comparison with final yr.

The slowdown in spending must also show useful to OI margins, which Anmuth expects will enhance because the yr progresses.

“Macro components will take longer to play out,” added the 5-star analyst, “however the firm has raised Prime costs & launched a gasoline surcharge to offset, & we anticipate AMZN to develop into its upfront spending extra in 2H22.”

Elsewhere, AWS noticed out Q1 with a backlog of $88.9 billion – its greatest ever – whereas development accelerated to 68% year-over-year. Anmuth thinks 30%+ AWS income development is “sustainable” in 2022, and as comps ease, Promoting must also see a major uptick.

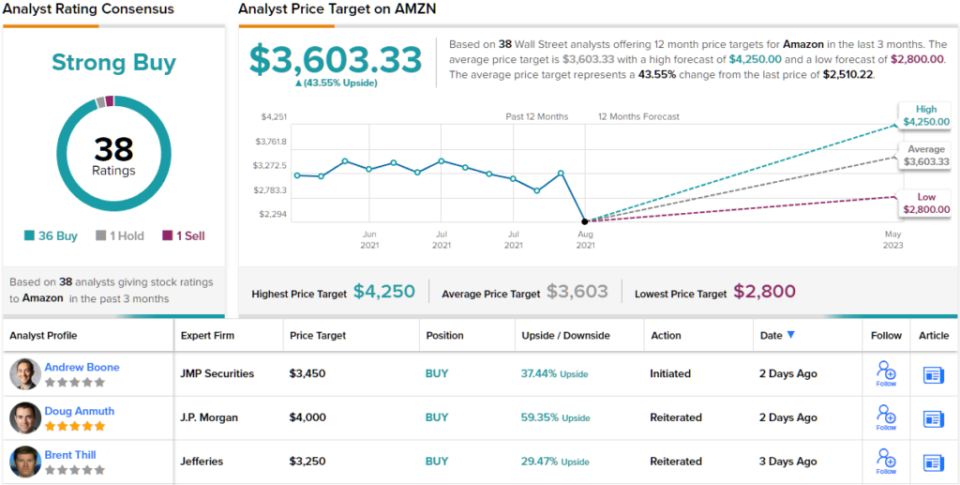

All in all, Anmuth calls Amazon his “Greatest Concept,” and reiterated an Obese (i.e., Purchase) ranking together with a $4,000 worth goal. The implication for traders? Upside of 59%. (To observe Anmuth’s observe report, click on right here)

The Road’s cadre of analysts virtually unanimously agree; of the 38 critiques on file, 36 are to Purchase, making the consensus view on this inventory a Sturdy Purchase. Going by the common goal of $3,603 and alter, shares are anticipated to climb ~44% increased within the yr forward. (See Amazon inventory forecast on TipRanks)

To search out good concepts for shares buying and selling at engaging valuations, go to TipRanks’ Greatest Shares to Purchase, a newly launched device that unites all of TipRanks’ fairness insights.

Disclaimer: The opinions expressed on this article are solely these of the featured analyst. The content material is meant for use for informational functions solely. It is vitally essential to do your personal evaluation earlier than making any funding.

[ad_2]

Source link