[ad_1]

(Bloomberg) — US equity-index futures and European bonds fell as traders nervous concerning the twin threats of dwindling financial development and cussed inflation.

Most Learn from Bloomberg

Contracts on the S&P 500 and Nasdaq 100 dropped 0.3% every after the underlying indexes capped their eleventh decline in 13 weeks. European shares rose for the primary time in 4 days as dip-buyers emerged. The greenback weakened in the beginning of the US Independence Day vacation after a report the US could ease tariffs on China. Italian bonds tumbled with traders watching home political tensions.

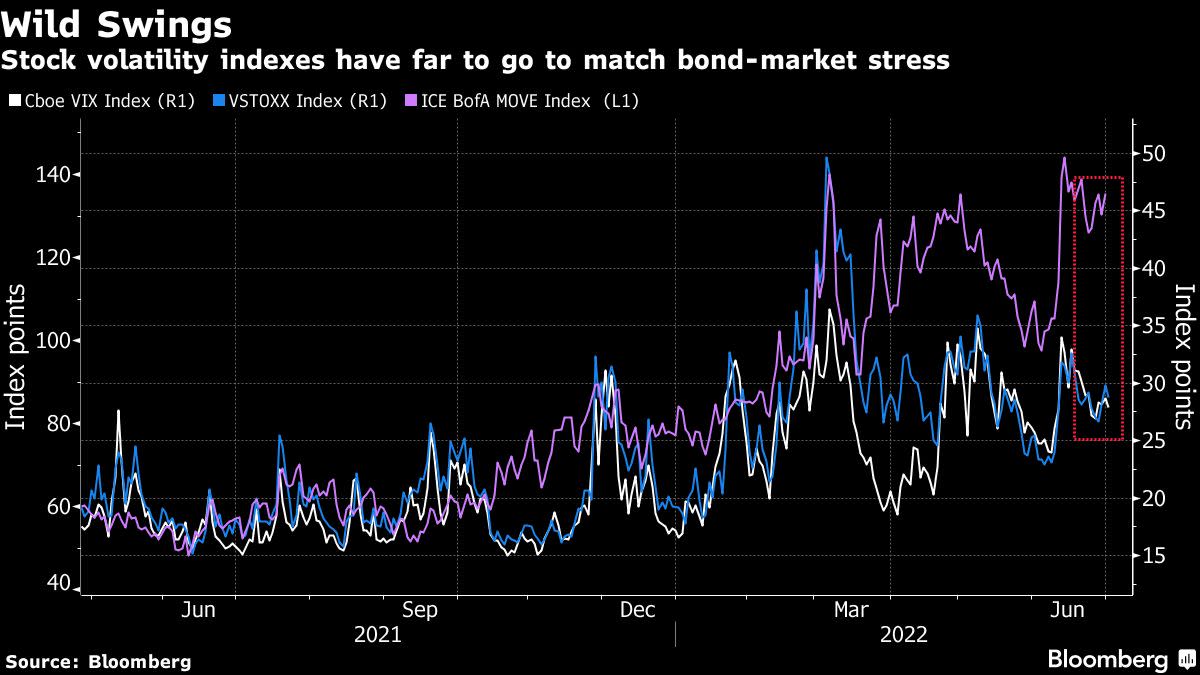

World shares and bonds are within the grip of the worst selloff in not less than three many years as rising possibilities of a US — and even international — recession are spooking traders. On the identical time, sticky inflation has left little room for the Federal Reserve to use brakes on financial tightening. This poisonous mixture presents markets a buying and selling problem not seen because the late Seventies.

“The market has begun to fret extra about financial development than simply liquidity withdrawal and inflation,” Stephen Innes, managing companion at SPI Asset Administration, wrote in a notice. “In contrast to earlier downturns, inflation is way greater and unemployment is way decrease. These dynamics delay any potential dovish central-bank pivot regardless of the speedy shift in front-end price expectations over the previous week.”

The MSCI All-Nation World Index, the worldwide benchmark, plunged 21% within the first half, the worst year-to-date losses since not less than 1988. Equally, the 14% loss within the Bloomberg International Combination Index of investment-grade debt was its worst efficiency since 1990, the earliest date for which data can be found.

The greenback slipped Monday, sending the euro and British pound 0.3% greater. US President Joe Biden could announce the rolling again of some tariffs on Chinese language imports as quickly as this week, Dow Jones reported.

In Europe, the Stoxx 600 benchmark climbed 0.7%. Vitality, commodity and journey shares had been the most important gainers.

Italian bonds slid earlier than a gathering between Prime Minister Mario Draghi and 5 Star chief Giuseppe Conte to settle weeks of political tensions. The nation’s 10-year yield jumped 12 foundation factors to three.21%, widening its unfold over German bunds to 1.90 share factors.

In China, officers had been making an attempt to repel a Covid flareup that might buffet an economically vital area. That’s one other take a look at of Beijing’s technique of making an attempt to remove the pathogen with mass testing and disruptive lockdowns.

Individually, developer Shimao Group Holdings Ltd. stated it didn’t pay a $1 billion greenback notice that matured Sunday, among the many greatest greenback cost failures up to now this 12 months in China.

Crude oil traded regular round $108 a barrel and Bitcoin hovered above the $19,000 stage.

What to observe this week:

-

Australia price determination, Tuesday

-

PMIs for euro space, China, India amongst others, Tuesday

-

US manufacturing unit orders, sturdy items, Tuesday

-

FOMC minutes, US PMIs, ISM providers, JOLTS job openings, Wednesday

-

EIA crude oil stock report, Thursday

-

Fed Governor Christopher Waller, St. Louis Fed President James Bullard, scheduled to talk, Thursday

-

ECB account of its June coverage assembly, Thursday

-

US employment report for June, Friday

Among the essential strikes in markets:

Shares

-

Futures on the S&P 500 fell 0.3% as of 6:48 a.m. New York time

-

Futures on the Nasdaq 100 fell 0.3%

-

Futures on the Dow Jones Industrial Common fell 0.2%

-

The Stoxx Europe 600 rose 0.9%

-

The MSCI World index rose 0.4%

Currencies

-

The Bloomberg Greenback Spot Index fell 0.2%

-

The euro rose 0.4% to $1.0451

-

The British pound rose 0.3% to $1.2132

-

The Japanese yen fell 0.2% to 135.42 per greenback

Bonds

Commodities

-

West Texas Intermediate crude was little modified

-

Gold futures rose 0.3% to $1,806.50 an oz

Most Learn from Bloomberg Businessweek

©2022 Bloomberg L.P.

[ad_2]

Source link